NATURAL CAPITAL - AUSTRALIA

EXPERIMENTAL ENVIRONMENTAL ACCOUNTING AT THE NATIONAL LEVEL

|

TPB / TVM COMMENTARY

Australia has been at the forefront of national level statistics and government financial management for several decades ... and it comes at no surprise that they are doing significant work in the area of environmental accounting. I am struck by the high environmental value that is placed on energy resources, which I believe is a result of valuing resources using money as a single composite unit of account. Timber has virtually no value, while fossil based energy resources have a very high valuation.

|

|

INTEGRATED SOCIOECONOMIC AND ENVIRONMENTAL INDICATORS

|

|

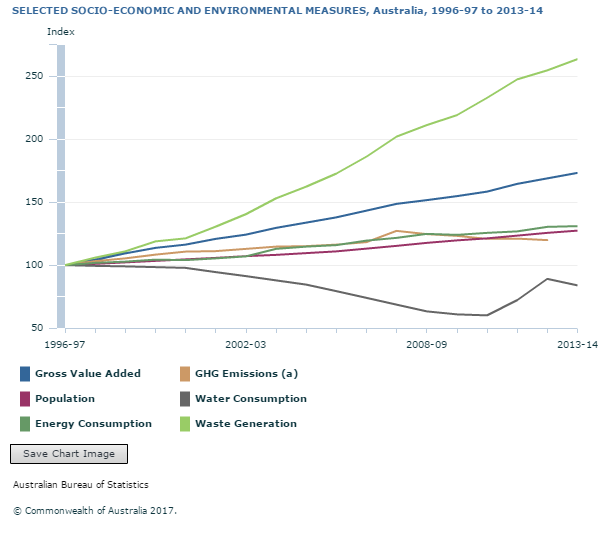

ECONOMIC PRODUCTION AS MEASURED BY GVA

Australia's economic production, as measured by Gross Value Added (GVA) in chain volume terms, rose 73% over the period 1996-97 to 2013-14.

Over the same period, indicators of environmental pressure related to the production of waste, energy consumption and greenhouse gas (GHG) emissions all increased, while water consumption fell.

Waste production rose 163%, energy consumption increased 31% and GHG emissions increased 20%.

Water consumption in Australia has fallen by 16% since 1996-97. However, the increase in water availability over the most recent years, due to higher rainfall, has supported a rise in water consumption (an increase of 40% between 2010-11 and 2013-14) and in turn led to a recent increase in the intensity of water use by industry.

Annotation(s): Index: 1996-97 = 100

Footnote(s): (a) Timeseries runs to 2012-13.

Source(s): Australian Environmental-Economic Accounts

|

|

|

INDICATORS OF ENVIRONMENTAL PRESSURE FOR SELECTED INDUSTRIES

Environmental pressure refers to human activities that place pressure on the environment, for example, manufacturing activity giving rise to pollutants. The measures contained in this section provide an indication of environmental pressure for selected industries.

A comparison of changes in selected indicators of environmental pressure per unit of economic production (GVA) between 1996-97 and 2013-14 illustrates, among other things, the close correlation between Australia's GHG emissions intensity and energy intensity (footnote 1). Both followed a similar downward trend with GHG emissions intensity declining by 29% between 1996-97 and 2012-13, while energy intensity fell by 24% between 1996-97 and 2013-14.

Waste intensity is the only reported indicator of intensity to increase between 1996-97 and 2013-14 (52%). This result is consistent with international evidence which suggests that economic growth is associated with growth in waste production per capita (footnote 2).

Annotation(s): Index: 1996-97 = 100

Footnote(s):

(a)Timeseries runs to 2012-13.

Source(s): Australian Environmental-Economic Accounts

|

|

|

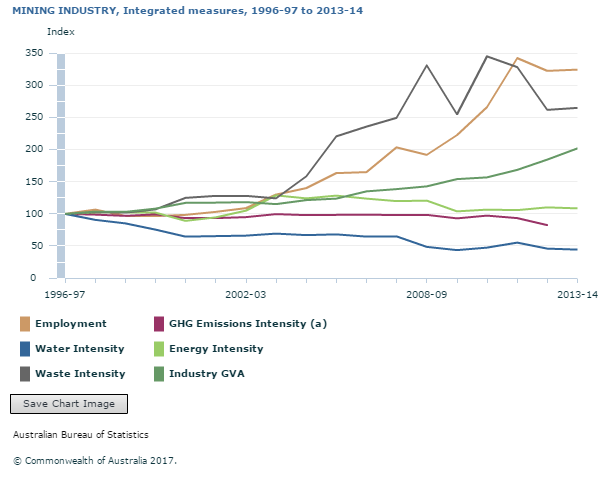

Mining

The value of mining production as measured by GVA increased steadily between 1996-97 and 2013-14, to finish the period up 102% from $65b to $130b. The mining industry's share of total GVA rose from 8% in 1996-97 to 9% in 2013-14. This increase was accompanied by a proportionately larger rise in the number of persons employed in the mining industry, up 224% from 80,500 in 1996-97 to 261,000 in 2013-14.

Annotation(s): Index: 1996-97 = 100

Footnote(s): (a) Timeseries runs to 2012-13.

Source(s): Australian Environmental-Economic Accounts

The indicators of environmental pressure for the mining industry reveal a mixed picture. The energy consumed per unit of economic production (energy intensity) by the industry was variable between 1996-97 and 2013-14. After falling early in the period, the energy intensity of mining rose 35% between 2000-01 and 2005-06, then declined thereafter to finish 9% higher over the full 18-year period.

The mining industry increased its focus on lower value (dollar per tonne) commodities, such as coal and iron ore during the early-to-mid 2000s. This resulted in a relatively greater level of energy use for extraction and processing than for commodities with higher unit values (i.e. more tonnes must be removed in order to generate the same value of production). Part of this relates to the higher proportion of production coming from open cut mines. This method typically requires removal of large quantities of soil, rock and so on (i.e. overburden) to expose the commodity, with a corresponding increase in energy use for overburden removal, before commodity production begins.

For the mining industry, waste intensity recorded the greatest increase among the indicators of environmental pressure, increasing 165% in the 18-year period to 2013-14. The majority of this increase occurred between 2003-04 and 2010-11 when waste intensity rose by 177%. This period coincides with a rapid expansion of the mining industry, with the opening and expanding of mines contributing to a major proportion of waste production in the mining industry. Similarly, the clean-up of laydown yards, historic waste stockpiling and demolition of closed mines produced large amounts of waste.

GHG emissions intensity recorded by the mining industry decreased by 17% for the period 1996-97 to 2012-13 and water intensity decreased by 56% for the period 1996-97 to 2013-14.

|

|

|

Agriculture

The value of production generated by the agriculture industry (including forestry and fishing), as measured by its GVA, rose from $24b to $36b between 1996-97 and 2013-14. The agriculture industry's contribution to total GVA across all industries fell from 3% in 1996-97 to 2% in 2013-14. This decrease was accompanied by a 20% drop in employment in the agriculture industry, from 403,500 in 1996-97 to 324,500 in 2013-14.

Annotation(s): Index: 1996-97=100

Footnote(s): (a) Timeseries runs to 2012-13.

Source(s): Australian Environmental-Economic Accounts

The agriculture industry witnessed a steady trend downwards in water intensity, decreasing 67% over the period 1996-97 to 2009-10. In response to the drought dominated climatic conditions of the early 2000's, the agriculture industry became more efficient with water use through infrastructure improvements, technology advancements and changes to crop selection. Between 2009-10 and 2013-14, however, increased water availability resulting from higher rainfall accompanied a 56% rise in the volume of water consumed per unit of economic output produced by the agriculture industry.

The energy intensity of the agriculture industry increased 40% over the 18 years to 2013-14. Energy consumed per unit of economic production by agriculture was variable over the whole period from 1996-97 to 2013-14, primarily due to swings in the industry’s economic output. GHG emissions intensity was similarly variable, rising 18% in the decade to 2007-08, before falling thereafter to finish down by 26% across the entire recorded period. In contrast, waste production by agriculture recorded a 32% increase in intensity between 1996-97 and 2013-14.

|

|

|

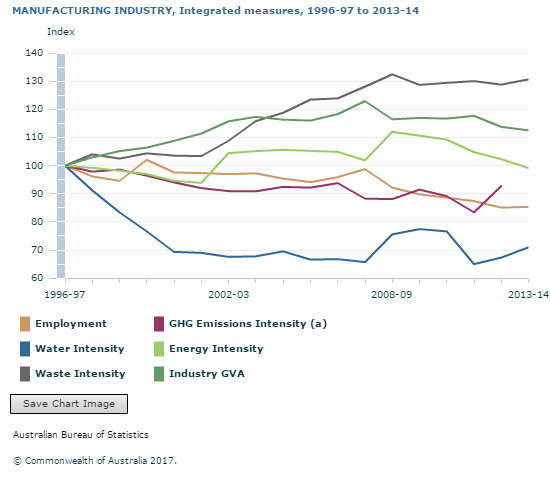

Manufacturing

GVA of the manufacturing industry rose 13% between 1996-97 and 2013-14 from $90b to $102b. However, the industry's contribution to total GVA fell from 11% in 1996-97 to 7% in 2013-14. The number of persons employed in the manufacturing industry also fell, from 1,075,200 in 1996-97 to 917,600 in 2013-14.

Annotation(s): Index: 1996-97 = 100

Footnote(s):

(a) Timeseries runs to 2012-13.

Source(s): Australian Environmental-Economic Accounts

The energy intensity of the manufacturing industry was flat across the period 1996-97 and 2013-14, while the GHG emissions intensity for the industry declined 7% over the slightly shorter 1996-97 to 2012-13 period. Waste intensity for the manufacturing industry increased 31% between 1996-97 and 2013-14.

|

|

|

ENVIRONMENTAL ASSETS

|

|

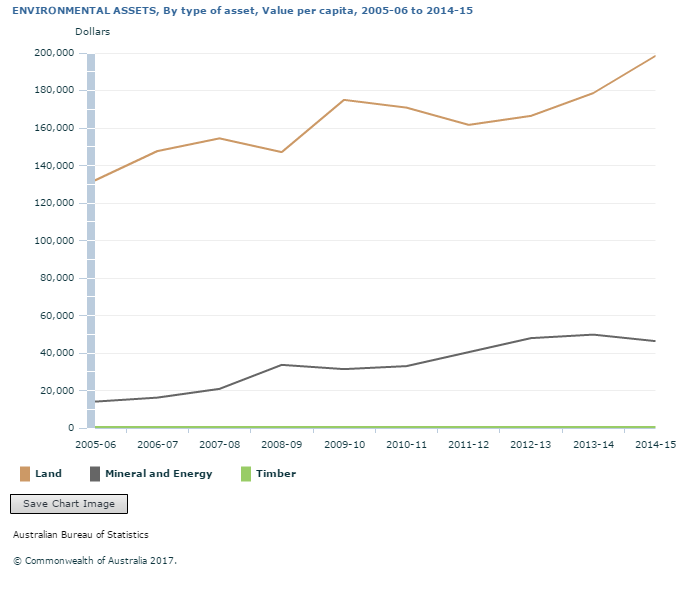

ENVIRONMENTAL ASSETS

The notion of environmental assets used in this publication is consistent with the System of Environmental-Economic Accounting 2012 (SEEA) definition and can include: subsoil assets, both mineral and energy; land; soil resources; timber resources, both plantation and native forest; aquatic resources (e.g. fish), both cultivated and natural; water resources, comprising surface water, ground water and soil water; and other biological resources. The ABS makes estimates of the value of subsoil, land and timber assets. While the ABS does not currently estimate the value of all water resources or aquatic resources, these are the subject of ongoing research.

The value of Australia’s environmental assets (in current prices) increased 95% over the period 2005-06 to 2014-15 from $2,999.5b to $5,837.5b. The value of Australia’s produced capital also increased over this period, although to a lesser extent (70%), rising from $3,276.7b to $5,564.1b. Environmental assets now make up the largest share of Australia’s capital base.

Source(s): Australian Environmental-Economic Accounts

|

|

|

Overview of changes in environmental assets

In 2014-15 land accounted for 81% of the value of Australia's environmental assets, down from 90% in 2005-06. Over the same period, the value of land (in current prices) increased 75% to $4,722.2b.

The share of mineral and energy resources among Australia’s environmental assets rose from 10% to 19% in the decade to 2014-15.

This occurred alongside a 282% rise in the value of mineral and energy resources from $288.6b in 2005-06 to $1,103.5b in 2014-15, a change that is further described below.

Source(s): Australian Environmental-Economic Accounts

|

|

|

Timber assets

The value of Australia's timber assets grew by 18% between 2005-06 and 2014-15. Australia's timber assets are comprised of: native standing timber, which decreased in value by 14% to $1.8b in the decade to 2014-15; and plantation standing timber, which rose in value by 27% to $10.0b for the same period. Throughout this period, the value of Australia’s timber assets remained at less than 1% of the total value of Australia's environmental assets.

The value of produced capital on a per capita basis increased in current price terms by 46% from $160,222 in 2005-06 to $233,971 in 2014-15. The value of Australia’s stock of environmental assets on a per capita basis increased by 67% over the same period, from $146,668 in 2005-06 to $245,467 in 2014-15.

Source(s): Australian Environmental-Economic Accounts

|

|

|

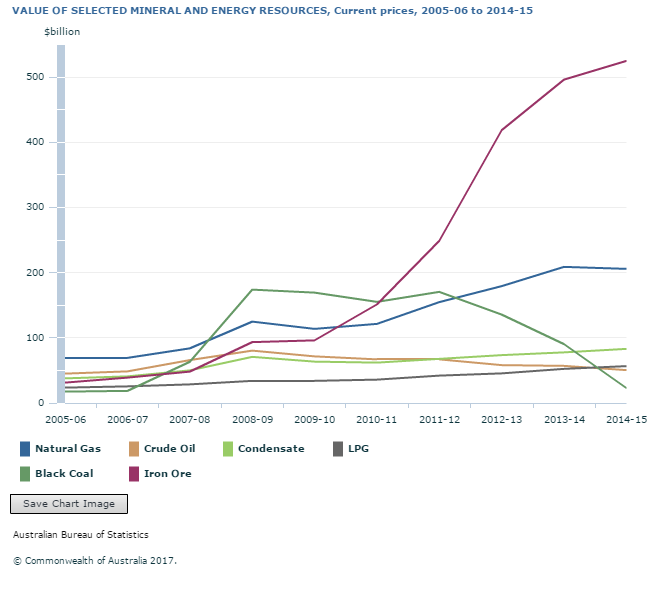

Mineral and energy resources

Strong overseas demand for mineral and energy resources, particularly from China, drove a boom in the prices of many of these resources over much of the decade to 2014-15. These price rises increased the economic viability of many mineral and energy resources and led to increases in the amount of resources assessed as being within the scope of economically demonstrated resources (EDR) for these mineral and energy assets (footnote 3).

Source(s): Australian Environmental-Economic Accounts

Between 2005-06 and 2014-15, the value of Australia’s iron ore assets rose from $31.5b to $524.9b as a direct result of increased market prices. In turn, the proportion of the value of total mineral and energy resources attributable to iron ore rose from 11% to 48% over the decade to 2014-15.

Among other categories of mineral and energy resources, notable increases in the physical quantity of EDR between 2005-06 and 2014-15 were reported for rare earths (538%), copper (106%), silver (90%) and gold (64%). Lithium recorded the largest percentage rise in physical EDR, with stocks rising 800% over the decade to 2014-15.

For bauxite resources, estimates of physical quantity rose 5% from 5.8Gt to 6.1Gt over the 10 years to 2014-15. However, for this period, the value of Australia's bauxite assets fell considerably (91%) from $12.6b to $1.1b. This fall occurred against a backdrop of an over-supply of aluminium, of which bauxite is the most important ore, and increased refining costs.

In 2014-15, the physical extent of Australia’s energy resources was estimated at 62Gt for black coal; 44Gt for brown coal; 1,143Kt for uranium; 2,600bcm for natural gas; 128GL for crude oil; 254GL for condensate; and 120GL for liquefied petroleum gas (LPG).

Black coal EDR increased significantly between 2005-06 and 2014-15 mainly due to new discoveries and through reclassification of existing resources. Australia's physical stocks of black coal rose 58% over the decade to 2014-15. This was accompanied by a 33% increase in the value of black coal from $17.5b to $23.2b.

Between 2005-06 and 2008-09, the value of Australia's uranium deposits increased from $0.3b to $0.9b. Since 2008-09, however, the economic value of uranium has fallen in line with falls in international prices for uranium. While physical stocks of uranium have remained relatively stable (1,143Kt in 2014-15), the value of these resources declined from $0.9b in 2008-09 to $0.2b in 2014-15, a fall of 78%.

All categories of petroleum resources rose in value between 2005-06 and 2014-15. Natural gas increased by 199%, LPG by 140%, condensate 120% and crude oil 11%. In contrast, changes in physical quantities for these stocks between 2005-06 and 2014-15 was a mixture of increases and falls, with the stock of natural gas rising by 8% and condensate by 14%, while LPG and crude oil declined by 39% and 23% respectively.

Footnote(s):

(a) Economically demonstrated resources.

Source(s): Australian Environmental-Economic Accounts

|

|

|

Energy (PJ) content

In terms of energy (PJ) content, black coal was Australia's most significant energy resource throughout the period 2007-08 to 2013-14, with an estimated energy content of 1,676,700PJ (or 58% of total) as at 30 June 2014. In terms of energy content, Uranium was the second most significant energy resource (649,040PJ or 23% of total), followed by brown coal (433,160PJ or 15%).

|

|

|

WATER SUPPLY, USE AND CONSUMPTION

|

|

Water consumption

Water consumption is the amount of water used in the economy. It refers to water that has entered the economy, but has not been returned to either water resources or the sea. Total water use differs from water consumption, because water use includes in-stream use (such as that used in hydro electricity generation) and water supplied to other users and the environment.

Australian water consumption in 2013-14 was 18,645GL, a decrease of 6% or 1,111GL from 2012-13. While water consumption declined between 2008-09 and 2010-11, the subsequent large increase between 2010-11 and 2013-14 was mainly driven by a 61% or 4,464GL increase in water consumption by the agriculture industry (including forestry and fishing).

Footnote(s):

(a) Includes Forestry and Fishing.

(b) Includes Gas.

(c) Includes Waste Services.

Source(s): Australian Environmental-Economic Accounts

The agriculture industry was the largest consumer of water throughout the six years from 2008-09 to 2013-14, consuming 11,814GL of water in 2013-14. Between 2008-09 and 2010-11 water consumption by the agriculture industry was steady at around 7,300GL per annum. Water consumed by the agriculture industry increased by 4,464GL between 2010-11 and 2013-14, with the three most significant contributors to this increase being: dairy cattle farming; sheep, beef and grain farming; and other crop growing. In combination these three activities made up 83% of total water consumed by the agriculture industry in 2013-14.

Water consumption by water supply, sewerage and drainage services industry fluctuated between 2008-09 and 2013-14. It decreased by 32% between 2008-09 and 2010-11, before increasing by 47% between 2010-11 and 2013-14. A significant proportion of water consumed by the water supply industry relates to leakages from water distribution networks.

Water consumption by the manufacturing industry was steady at approximately 650GL per annum over the three years to 2010-11, and then decreased by 11%, or 70GL, from 2010-11 to 2013-14. The reduction was driven by the wood, pulp, paper and converted paper product industry and the food, beverage and tobacco product industry consuming less water.

Elsewhere, water consumption patterns were more mixed. The mining industry increased its water consumption by 29% (from 506GL to 652GL between 2008-09 and 2013-14) while water consumed by households increased only slightly (3%) over the same period.

Between 2008-09 and 2013-14, the agriculture industry increased its share of total water consumed in the Australian economy from 52% to 63%. Manufacturing’s share of water consumption dropped from 5% in 2008-09 to 3% in 2013-14. Other industries to decrease their share of total water consumption over the same period included mining (down from 4% in 2008-09 to 3% in 2013-14) and water supply, sewerage and drainage services (down from 16% in 2008-09 to 12% in 2013-14).

Household consumption

Households’ share of total water consumption in Australia decreased from 13% in 2008-09 to 10% in 2013-14. Over the same period, water consumption by households increased 3% from 1,818GL in 2008-09 to 1,872GL in 2013-14.

The average price paid for water by Australian households has increased by $1.20/KL or 74% between 2008-09 and 2013-14, from $1.63/KL to 2.83/KL. South Australia had the highest average water price in 2013-14 at $4.25/KL (up 93% from 2008-09), followed by Victoria at $3.39/KL (up 109% from 2008-09) and Tasmania at $3.11/KL (up 148% from 2008-09). The Northern Territory had the lowest average water prices for households at $1.62/KL.

|

|

|

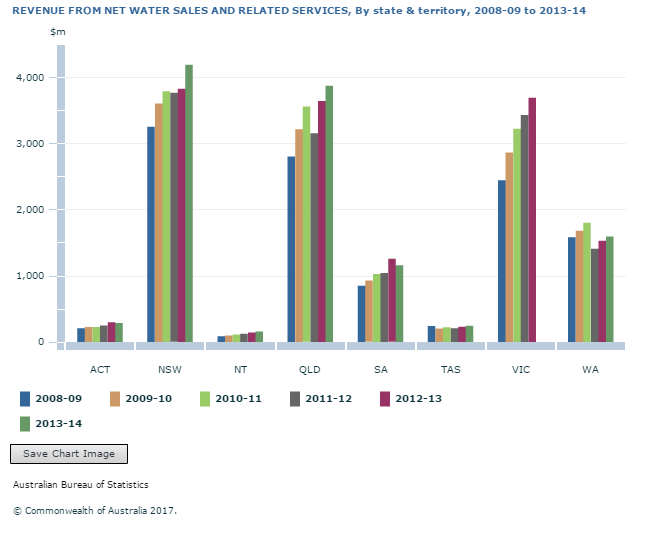

Water revenue and expenditure

Total revenue from sales of water and related services by the water supply industry increased from $11,481m to $16,072m (or 40%) between 2008-09 and 2013-14. The water supply industry accounted for 99% of total water revenue throughout the six years to 2013-14.

Of the total water and related services revenue collected by the water supply industry in Australia in 2013-14, Victoria collected the highest proportion of any state (28%, an increase from 21% in 2008-09), followed by New South Wales (26%, a decrease from 28% in 2008-09) and Queensland (24%, unchanged from 2008-09).

Source(s): Australian Environmental-Economic Accounts

|

|

|

Water Use in monetary and physical units

A comparison of relative use (in physical terms) and expenditure (in monetary terms) of distributed and reuse water across industries and households shows that, as of 2013-14, agriculture uses the most distributed and reuse water (58% of total) and pays comparatively less for it (6% of total water expenditure). In comparison, households use relatively less water (13% of total distributed and reuse water) and account for 53% of the total expenditure on water. While data on types of distributed and reuse water (i.e. potable and non-potable) are not available, water paid for and used by the agriculture industry is almost entirely non-potable.

During the six year period to 2013-14, agriculture’s share of total expenditure on distributed and reuse water remained relatively stable (6% in both 2008-9 and 2013-14), while the industry’s share of total water use increased from 40% to 58%. Households share of total expenditure on distributed and reuse water increased from 45% in 2008-09 to 53% in 2013-14, while the sector’s share of total water use decreased from 18% to 13% over the same period.

Footnote(s):

(a) Distributed and Reuse water.

(b) Includes Forestry and Fishing.

(c) Electricity and Gas.

(d) Water and Waste Services.

Source(s): Australian Environmental-Economic Accounts

The agriculture industry paid $0.08 per kilolitre (KL) in 2013-14 compared to mining ($2.00/KL), electricity and gas ($0.84/KL) and other industries ($1.37/KL). In explaining these differences, water used by agriculture is typically transported through open waterways and channels and the value of this infrastructure is less than that needed for potable water.

|

|

|

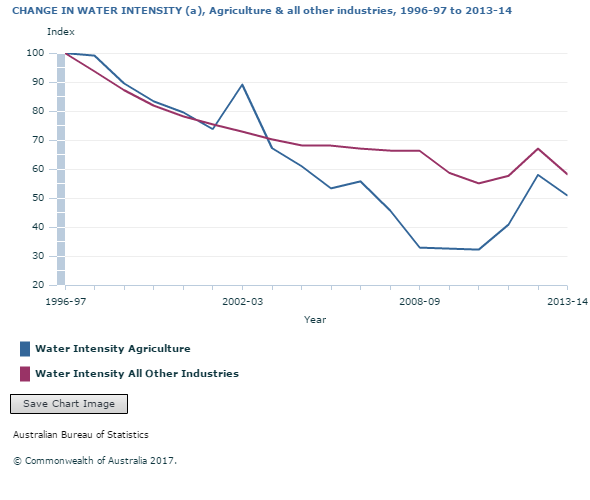

Industry intensity of water use

Water intensity is a measure of the water consumed to produce one unit of economic output. It is calculated by dividing water consumption by Industry Gross Value Added (GL/ GVA). The volume of water required by the agriculture industry to produce one unit of economic output fell by 68% between 1996-97 and 2010-11 to 0.21GL/ GVA. Since then, the water intensity of Agriculture has increased 58% to 0.33GL/ GVA against a backdrop of easing drought conditions. The water intensity of all other industries declined by 42% between 1996-97 and 2013-14.

Annotation(s): Gross Value Added in chain volume terms. Index: 1996-97 = 100.

Footnote(s): (a) Intensity equals GL water / GVA.

Source(s): Australian Environmental-Economic Accounts

Gross value of irrigated agricultural production

Total gross value of irrigated agricultural production (GVIAP) for Australia in 2013-14 was $14.6b, up 22% from 2008-09. The three commodities with the highest GVIAP in Australia in 2013-14 were dairy ($2.7b, up 21% from 2008-09) fruit excluding grapes ($2.7b, up 14% from 2008-09), and vegetables ($2.5b, down 4% from 2008-09).

Rice and cotton, which are the most water intensive crops, have seen significant increases in GVIAP between 2008-09 and 2013-14 increasing by 689% and 214% respectively. Other products recording an increase between 2008-09 and 2013-14 include: production of sheep and other livestock (253%); production from meat cattle (58%); and sugar cane (19%).

Total GVIAP for cereals grown for grain and seed decreased 50% or $157m between 2008-09 and 2010-11. Since then, GVIAP for cereals has increased consistently to finish the six years to 2013-14 up 28%. Total GVIAP for grapes decreased steadily between 2008-09 and 2013-14 and reported an overall decline of 24% for this period.

|

|

|

ENERGY SUPPLY AND USE

|

|

Supply of energy

Between 2008-09 and 2013-14, Australia’s total net supply of energy increased by 5% from 19,924PJ to 20,992PJ. Net supply of energy accounts for the transformation of primary energy products to secondary energy products and related conversion losses. Thus net supply of energy avoids double-counting amounts of converted primary energy.

In 2008-09, 91% of total net supply was produced domestically and the remainder (9%) was imported. This pattern has been largely stable throughout the six-year period following 2008-09. In 2013-14, 90% of total net supply was produced domestically, with the remaining 10% from imports.

Mining was the main producer of domestic energy throughout the period from 2008-09 to 2013-14, principally through the extraction of fossil fuels and uranium. The industry’s contribution to total domestic net energy supply was 86% (or 17,165PJ) in 2008-09, declining slightly to 85% of total supply (or 17,937PJ) in 2013-14. Relative shares of net energy supplied to the Australian economy by other industries and imports also remained relatively constant over this period.

Black coal accounts for the largest share of domestic production of energy in Australia. It has maintained its share of total domestic production at 50% across both 2008-09 (9,009PJ) and 2013-14 (11,807PJ). In contrast, uranium has fallen from 27% (or 4,846PJ) of total domestic production in 2008-09 to 14% (or 2,608PJ) in 2013-14.

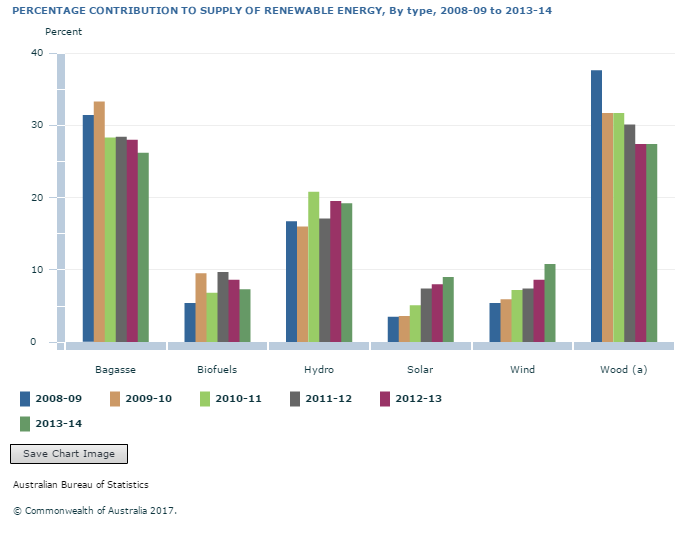

Renewable energy production increased 33% (or 85PJ) between 2008-09 and 2013-14, although its contribution to total net energy supply rose from just 1% to 2%. Solar recorded the largest increase in production, rising 244% from 9PJ in 2008-09, to 31PJ in 2013-14. Wood and wood waste was the only category of renewable energy to decrease production levels between 2008-09 and 2013-14, falling by 3%.

Footnote(s): (a) Includes Wood Waste.

Source(s): Australian Environmental-Economic Accounts

Imports of energy products increased by 19% from 1,750PJ in 2008-09 to 2,087PJ in 2013-14. The most significant energy import is crude oil and refinery feedstock, which represented 940PJ or 54% of total energy imports in 2008-09, increasing to 1,096PJ or 53% in 2013-14. Imports of refined fuels increased by 27% from 661PJ in 2008-09 to 841PJ in 2013-14 and among these products, diesel imports became markedly more predominant. Across the period between 2009-09 and 2013-14, diesel imports rose by 65% from 318 PJ to 525 PJ while imports of other refined products (including petrol) declined by 8% from 343PJ to 316PJ.

|

|

|

Use of energy

Between 2008-09 and 2013-14, Australia’s domestic net energy use (i.e. by industry, households and government, but excluding exports) increased by 9% from 3,722PJ to 4,054PJ.

Net energy use by industry increased by 285PJ or 10% between 2008-09 and 2013-14, from 2,715PJ to 3,000PJ. Net energy use by industry as a percentage of total domestic energy use also increased marginally from 73% to 74% over the same period. The main energy sources used by industry are diesel (797PJ or 27% of energy used by industry in 2013-14, compared with 627PJ or 23% in 2008-09), natural gas (623PJ or 21% of energy used by industry in 2013-14, compared with 563PJ or 21% in 2008-09), and electricity (685PJ or 23% of energy used by industry in 2013-14, compared with 672PJ or 25% in 2008-09).

The household sector’s net energy use increased by 47PJ between 2008-09 and 2013-14 from 1,007PJ to 1,054PJ, though its relative share of total domestic energy use decreased slightly from 27% to 26% over the same period. The main fuel sources used by households are petrol (462PJ or 44% of total household energy use in 2013-14) and electricity (203PJ or 19% of total household energy use in 2013-14).

Manufacturing remains the largest user of energy among Australian industries. Despite this, the industry reduced its net use of energy from 994PJ in 2008-09 to 987PJ in 2013-14. Its relative contribution to total energy use by industry also declined from 37% to 33% over the same period. The relative shares of all other industries remained broadly unchanged during the six year period. In 2013-14, these shares included: transport 22% or 657PJ; mining 16% or 476PJ; commercial and services 15% or 446PJ; and construction 6% or 185PJ.

Footnote(s): (a) Includes Forestry and Fishing. (b) Includes Gas, Water and Waste Services. (c) Comercial and Services includes a range of service industries, including retail, wholesale, financial and health.

Source(s): Australian Environmental-Economic Accounts

|

|

|

Energy exports

Exports remain the largest net use of Australian energy products, accounting for 15,718PJ or 83% of domestic energy extraction in 2013-14, up from 13,784PJ or 76% in 2008-09. The main energy products exported are black coal (7,381PJ or 54% of energy exports in 2008-09, increasing to 10,578PJ or 67% in 2013-14) and uranium (4,754PJ or 34% of energy exports in 2008-09, decreasing to 3,149PJ or 20% in 2013-14). Natural gas exports rose during the period (from 838PJ or 6% of energy exports in 2008-09, to 1,267PJ or 8% in 2013-14). In contrast, crude oil and refinery exports declined over the same period (from 678PJ or 5% of energy exports in 2008-09, to 595PJ or 4% in 2013-14)

Footnote(s): (a) Includes coal seam methane, town gas and coal mine waste gas, excludes biogas. (b) Includes refinery feedstock, ethane and other petrochemical feedstocks.

Source(s): Australian Environmental-Economic Accounts

|

|

|

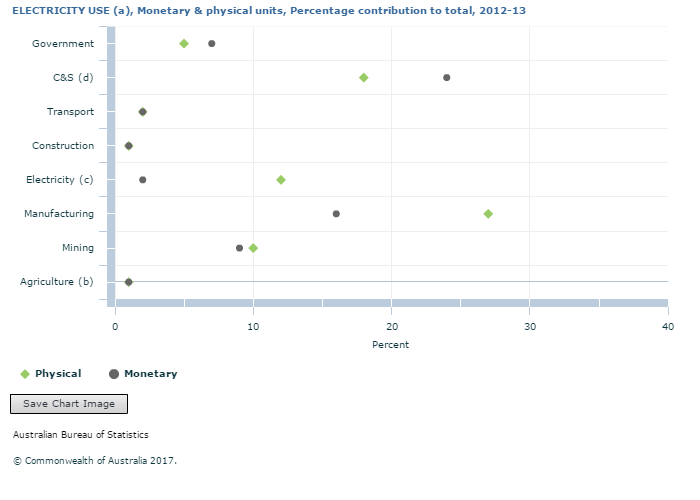

Electricity use and expenditure

In 2009-10, Australian industries and households paid $27,460m to use 908PJ of electricity, increasing to $40,763m (for 886PJ of electricity) in 2012-13.

The manufacturing industry was the largest user of electricity in all years from 2009-10 to 2012-13. In 2009-10, the Manufacturing industry consumed 258PJ (or 28% of total domestic use of electricity) and paid $4,720m for its electricity use (17% of total expenditure on electricity). In 2012-13, the industry consumed 242PJ of electricity (27% of total domestic use) and paid $6,481m (16% of total expenditure).

In contrast, households used 219PJ (or 24% of domestic use of electricity) in 2009-10, paying $10,820m (39% of total expenditure on electricity). By 2012-13, household use of electricity had declined to 207PJ (23% of total domestic consumption) while household expenditure had increased to $15,305m (38% of total expenditure on electricity).

Footnote(s):

(a) 'Electricity' includes solar, solar hot water, wind, hydro and other electricity.

(b) Includes Forestry and Fishing.

(c) Includes gas, water and waste.

(d) Comercial and services includes a range of service industries, including retail, wholesale, financial and health.

Source(s): Australian Environmental-Economic Accounts

|

|

|

WASTE GENERATION AND MANAGEMENT

|

|

Waste generation by industry and households

The Australian economy generated 53m tonnes of waste in 2010-11, which was a slight decrease (1%) from the previous year. The fall was driven by declines in waste generation by the electricity, gas and water (20%) and waste management services (19%) industries. Mining recorded the largest increase (127%) in waste generation over 2009-10 to 2010-11.

The construction industry generated the largest volume of waste in 2010-11 (14.5m tonnes, representing 27% of the total waste generated). This is a decrease of 10% from the previous year (16.0m tonnes, representing 30% of the total waste generated in 2009-10). The bulk of waste generated by construction is masonry and the industry produced 10.9 million tonnes (67%) of all masonry waste in 2010-11, a 2.8 million tonnes (or 21%) decrease from 2009-10.

Households produced 14.3 million tonnes of waste (or 27% of total waste generated) in 2010-11, an increase from 12.4 million tonnes (or 23% of total waste generated) from a year earlier.

Footnote(s):

(a) Includes Forestry, excludes Fishing.

Source(s): Australian Environmental-Economic Accounts

|

|

|

Waste management

There are three 'destinations' for Australia's waste: disposal to landfill; recovery for use in the domestic economy; and export.

Of the total waste generated in 2010-11, 30.8 million tonnes was recovered, which included 27.1 million tonnes recovered domestically and 3.7 million tonnes that was exported. Waste recovery (domestic and exports) increased from 52% of total waste generated in 2009-10 to 58% in 2010-11. Total waste to landfill decreased by 14% between 2009-10 and 2010-11 (from 25.9 million tonnes to 22.2 million tonnes).

Businesses and government provide waste management services that are used by other businesses, government and households. The monetary value of waste management services pertains to income from a range of services related to waste management, including collection, transport, recycling, treatment, processing or disposal of waste.

In 2010-11, the supply of these services was valued at $10.4b (including taxes), an 8% increase from 2009-10. Private waste management businesses (which include public trading enterprises) supplied just over half, $5.6b or 53%, of the value of these services, while local government authorities provided just over one quarter $2.7b, or 26%. The remaining $2.1b of waste management services was provided by businesses not primarily undertaking waste management, of which a large proportion (39% or $810m) were provided by the construction industry.

Waste management services are used by businesses in their production processes, or by households. In 2010-11, the waste management services industry consumed $3.2b, or 31%, of these services which was a slight increase from the year before ($2.9b, or 30%, in 2009-10). The construction industry was also a significant user of waste management services, consuming $1.8b or 18%. Households spent $1.9b on waste management services (recyclable and non-recyclable combined), mostly on municipal rates related to waste management services. Households’ share of total expenditure on waste management services remained unchanged at 18% between 2009-10 and 2010-11.

Footnote(s):

(a) Waste management services operated by private businesses (including public trading enterprises).

(b) Waste management services operated by local government authorities.

Source(s): Australian Environmental-Economic Accounts

In 2010-11, 60% or $3.2b of the total value of waste products supplied to the economy were consumed domestically with the remainder exported. Of those recyclable/recoverable materials exported, metal was the most valuable material at $1.8b in 2010-11, which represented a 34% increase from a year earlier.

Not all waste that is produced has a negative value. Where the owner/discarder of the waste materials receives payment for the waste, it is termed a waste product (e.g. paper and scrap metal). The value of waste products supplied to the economy increased 18% from $4.5b in 2009-10 to $5.4b in 2010-11. The waste management industry supplied 53% of the value of these products in the form of sales of raw materials (e.g. paper, cardboard, metals, organic materials etc.) in 2010-11 (up from 49% in 2009-10). The remaining 47% of waste products were supplied by industries that included mining ($327m, up 31% from 2009-10), manufacturing ($741m, up 2% from 2009-10), wholesale ($582m, up 6% from 2009-10) and retail ($565m, up 3% from 2009-10), which combined made up 89% of this remaining income from sale of waste products.

|

|

|

GREENHOUSE GAS EMISSIONS AND CARBON STOCKS

|

|

GREENHOUSE GAS EMISSIONS

All estimates of direct greenhouse (GHG) emissions contained in this publication are recorded on a SEEA basis i.e. on a residence basis. The residence basis differs from the territory basis, which underpins estimates of GHG emissions produced in accordance with the United Nations Framework Convention on Climate Change (UNFCCC).

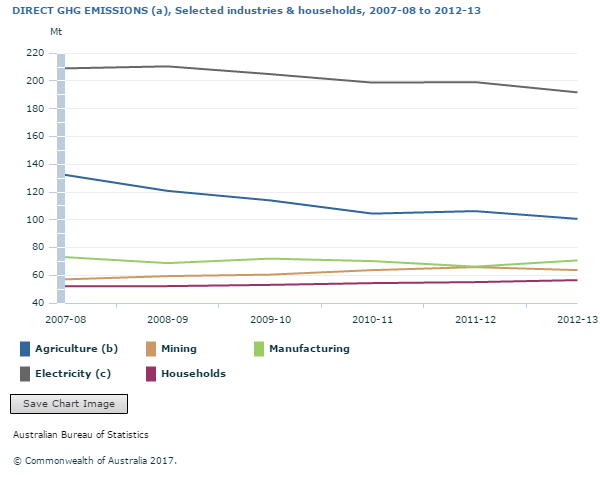

Total direct GHG emissions measured on a SEEA basis fell in every year from 2007-08 to 2010-11, rose slightly in 2011-12, before falling again in 2012-13. In the six years to 2012-13, total GHG emissions fell 6% from 595.3Mt of CO2 equivalent GHG emissions in 2007-08 to 561.4Mt in 2012-13. This decline can be largely attributed to the agriculture industry (including forestry and fishing) which recorded a fall in emissions of 31.6Mt (or 24%) between 2007-08 (132.3Mt) and 2012-13 (100.7Mt). The manufacturing industry also recorded a reduction in GHG emissions from 73.2Mt in 2007-08 to 70.7Mt in 2011-12 (i.e. a fall of 2.5Mt or 3%). Industries to increase their direct GHG emissions over the six years to 2012-13 included mining (up 12% to 63.8Mt), transport (up 10% to 40.3Mt) and construction (up 7% to 9.0Mt).

Footnote(s):

(a) SEEA basis.

(b) Includes Forestry and Fishing.

(c) Includes Gas, Water and Waste services.

Source(s): Australian Environmental-Economic Accounts

|

|

|

Contributors to GHG Emissions

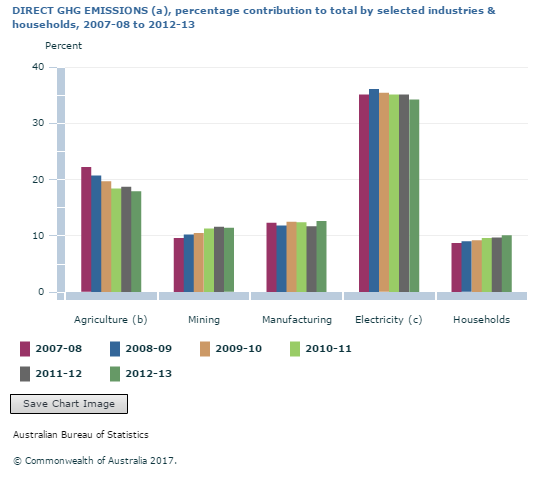

The electricity, gas, water and waste services industry was the most significant contributor to direct GHG emissions throughout the 2007-08 to 2012-13 period. In 2012-13 it produced 191.8Mt (or 34% of total direct GHG emissions) down from 209.1Mt (or 35% of total direct GHG emissions) in 2007-08. Other significant contributors to total GHG emissions in 2012-13 were: agriculture (which accounted for 18% of total GHG emissions, down from 22% in 2007-08); manufacturing (which accounted for 13% of total GHG emissions, up from 12% in 2007-08); and mining (which accounted for 11% of total GHG emissions, up from 10% in 2007-08).

GHG emissions generated by Australian households increased 9% from 52.0Mt in 2007-08 to 56.6Mt in 2012-13. Over the same period, households’ share of total direct GHG emissions increased from 9% in 2007-08 to 10% in 2012-13.

Footnote(s):

(a) SEEA basis.

(b) Includes Forestry and Fishing.

(c) Includes Gas, Water and Waste services.

Source(s): Australian Environmental-Economic Accounts

|

|

|

CARBON STOCK ACCOUNTS

This graph presents experimental estimates of carbon stocks in primary reservoirs in Australia. Carbon stock accounts report 239,581Mt of carbon stored in Australia’s geosphere. In comparison, 14,270Mt of carbon is stored as biomass carbon and 16,811Mt is stored as soil organic carbon.

Source(s): Australian Environmental-Economic Accounts

The estimates of Australia’s carbon stocks are experimental and are limited to the primary reservoirs of geocarbon and biocarbon. Geocarbon relates to carbon in the geosphere, and in this publication is further limited to fossil fuel resources. Biocarbon relates to carbon in the biosphere and includes all biomass and soil organic carbon to a depth of 30 cm (100 cm for marine ecosystems) irrespective of ecosystem type and land/water use. At present, carbon stocks contained within the Australian economy, for example, within concrete or plastics, are not covered in the experimental estimates.

|

|

|

ENVIRONMENTAL TAXES

|

|

ENVIRONMENTAL TAXES

In 2013-14, Australian governments levied environmental taxes of $36.7b, a similar level to 2012-13 ($36.3b), but an increase of $9.0b, or 33%, over the figure of $27.7b reported for 2011-12. The increase in the level of environmental taxes reported in 2012-13 and 2013-14 is primarily due to the introduction of the Carbon Pricing Mechanism ('carbon tax'), which came into operation on 1 July 2012. Commencing from the year 2014-15, the carbon tax is no longer levied by government.

Environmental taxes comprised 8% of total Australian tax revenue in 2013-14. In contrast, the previous decade saw the share of environmental taxes as a proportion of total tax revenue remain relatively constant at between 6 and 7%. Revenue from environmental taxes remained at around 2% of GDP throughout the 2003-04 to 2013-14 period.

Source(s): Australian Environmental-Economic Accounts

|

|

|

Environmental taxes by type of tax

The most significant environmental tax in Australia is the excise duty on crude oil, LPG and petroleum products, accounting for 48% of total environmental taxes in 2013-14. Between 2003-04 and 2013-14, this category of environmental taxes increased from $13.5b to $17.8b, a rise of $4.3b, or 32%.

The Carbon Pricing Mechanism raised $6.5b in its first year of operation (2012-13) and $6.9b in its second and final year of operation (2013-14). The scheme required entities which emitted over 25,000 tonnes per year of carbon dioxide equivalent greenhouse gases and which were not in the transport or agriculture sectors to obtain emissions permits.

Renewable energy certificates (RECs) fell by $0.3b between 2012-13 and 2013-14 (from $1.9b to $1.6b) but still recorded the greatest percentage rise among all categories of environmental taxes between 2003-04 and 2013-14, increasing 1,500% from $0.1b to $1.6b. Renewable energy targets (RETs) create a legal requirement for liable entities (typically electricity retailers) to purchase a set number of RECs and the observed changes in RECs is due directly to changes to the schedule of RETs.

Footnote(s):

(a) Carbon Pricing Mechanism.

(b) Renewable energy certificates.

(c) Passenger motor vehicles duty (import). (d) Stamp duty on vehicle registration.

Source(s): Australian Environmental-Economic Accounts

|

|

|

Environmental taxes paid by industry and households

The share of total environmental taxes paid by households was 26% in both 2012-13 and 2013-14, down from 32% in 2011-12. This fall in households' share of total environmental taxes is due to the introduction of the Carbon Pricing Mechanism, which is only levied on businesses. The value of environmental taxes paid by households rose by 39% between 2003-04 ($6.7b) and 2013-14 ($9.4b).

Electricity, gas and water supply industry paid more environmental taxes than any other industry in 2013-14, contributing $6.3b or 17% of all environmental taxes (up from $1.8b or 7% of all environmental taxes in 2011-12). This is primarily due to the industry’s obligations related to the Carbon Pricing Mechanism, with the electricity, gas and water supply industry in 2013-14 making 64% (or $4.4b) of total industry payments of this tax. The electricity, gas and water supply also made 98% (or $1.6b) of total RECs payments in 2013-14.

The commercial and services industry made the second highest industry contribution to total environmental taxes paid with $5.2b in 2013-14. The share of environmental taxes paid by this industry grew steadily between 2003-04 (14% of all environmental taxes) and 2011-12 (17% of all environmental taxes). Its share fell with the introduction of the Carbon Pricing Mechanism and was 14% of all environmental taxes in 2013-14.

In contrast, the mining industry increased its share of environmental taxes paid during this period from 6% (or $1.1b) in 2003-04 to 9% ($3.1b) in 2013-14. The increase was largely due to the effect of the Carbon Pricing Mechanism, and to a lesser extent the Mineral Resource Tax, both of which were introduced in 2012-13.

Footnote(s):

(a) Includes Forestry and Fishing.

(b) Includes Gas and Water supply.

(c) Comercial and Services includes a range of service industries, including retail, wholesale, financial and health.

Source(s): Australian Environmental-Economic Accounts

|

|

|

ENVIRONMENTAL EXPENDITURE ACCOUNTS

|

|

ENVIRONMENTAL EXPENDITURE ACCOUNTS

The Environmental Expenditure Account (EEA) describes the resources allocated for preserving and/or protecting the supply and use of services whose primary purpose is to reduce or eliminate pressures on the environment or to make more efficient use of natural resources. Consistent with the SEEA framework, the purpose of the EEA is to provide a framework and structure to identify these elements within the key aggregates of the System of National Accounts (SNA). Note that EEA results are experimental at this stage.

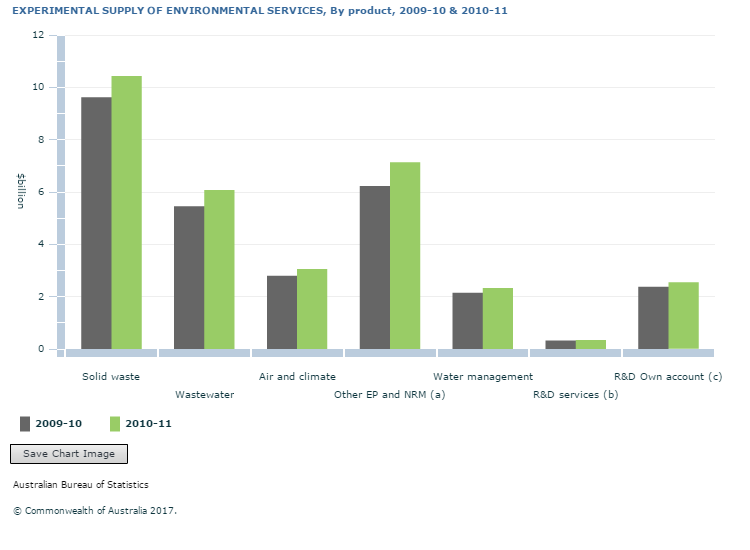

This graph shows the production of environmental-specific services by the type of environmental service being supplied.

Solid waste management services represented the largest share of total environmental services supplied within the Australian economy ($10.4b, or 33% of total environmental services in 2010-11, up 8% from $9.6b a year earlier). This was followed by waste water management ($6.1 billion, or 19% of total environmental services in 2010-11).

Footnote(s):

(a) Other Environmental Protection and Natural Resource Management.

(b) Research and Development Services.

(c) Research and Development Own account.

Source(s): Australian Environmental-Economic Accounts

|

|

|

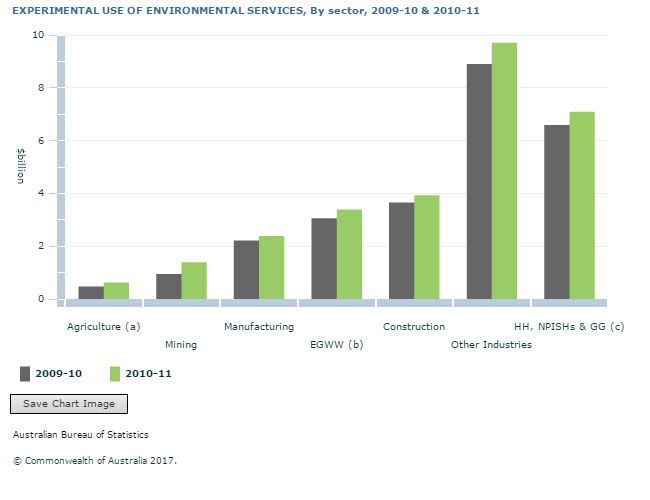

Experimental Use of Environmental Services

Experimental estimates of the use of environmental services by consumers within the Australian economy was valued at $28.5b (excluding capital formation) in 2010-11, an increase of 10% from 2009-10 ($25.9b). Australian industry consumed 75% (or $21.4b) of total environmental services in 2010-11, up from 74% (or $19.2b) in 2009-10.

The largest industry consumers of environmental services were construction ($3.9b in 2010-11, up 7% from $3.6b in 2009-10) and electricity, gas, water supply, drainage and sewerage and waste ($3.4b in 2010-11, up 11% from $3.1b in 2009-10).

Consumption of environmental services by households and general government increased by 8% between 2009-10 and 2010-11, from $6.6b to $7.1b.

Footnote(s):

(a) Includes Forestry and Fishing.

(b) Electricity, Gas, Water Supply, Drainage and Sewerage and Waste.

(c) Households, Non Profit Institutions Serving Households and General Government.

Source(s): Australian Environmental-Economic Accounts

|

|

|

LAND / LAND COVER

|

|

Land Cover Inventory

Experimental land cover accounts have been compiled for Australia for the periods January 2001 to December 2002 and January 2010 to December 2011 using Geoscience Australia's Dynamic Land Cover, beta version (DLCv2). A 10 year time interval was selected as the rate of change in land cover is slow and the supporting data set remains in a testing phase. As such the information should be interpreted cautiously and with reference to the data custodians Geoscience Australia.

This map presents land cover for the period January 2010 to December 2011, while the figure shows the changes between the periods January 2001 to December 2002 and January 2010 to December 2011.

The total land area of Australia is approximately 7.7m km2.

Herbaceous cover was the most abundant land cover in Australia in 2010-11 accounting for 3.6m km2 or 47% of all land cover, followed by Woody trees with 2.1m km2 or 28% and Woody-shrubs with 1.2m km2 or 15%.

Irrigated or rainfed cultivated land together represented 0.6m km2 or 8% of all land cover in January 2010 to December 2011.

There was little change in the area of irrigated or rainfed cultivated land between January 2001 to December 2002 and January 2010 to December 2011.

Woody-shrubs showed the greatest absolute increase between January 2001 to December 2002 and January 2010 to December 2011, growing by 0.4m km2, while the area of Wetlands increased by 85% or from 18,159 to 33,360 km2.

LANDCOVER, Australia, January 2010 - December 2011

Diagram: LANDCOVER, Australia, January 2010 to December 2011

|

|

|

Changes in land cover

Changes in land cover have many potential drivers, including human activities and natural phenomena. The DLCv2 data presented here summarises many observations of the Earth's surface to provide a single dominant land cover class for each of the two year periods selected. There will be some level of land cover change within and between each two year layer of DLCv2 caused by various drivers. This intra-period and inter-period variation should be considered when interpreting the changes reported between the periods January 2001 to December 2002 and January 2010 to December 2011. Examples of human activities that drive land cover change include urban development, crop and pasture management and industrial activity. Natural drivers of land cover change include flood events, bushfires and seasonal climatic variation.

Footnote(s): (a) This land cover category relates largely to urban land.

Source(s): Australian Environmental-Economic Accounts

|

|

|

|

FOOTNOTES

1 The intensity indicators presented in this publication are described in the Glossary.

2 Productivity Commission, 2006, Inquiry Report No. 38.

3 Economically demonstrated resources (EDR) is used to measure the physical extent of a given resource. EDR is a measure of the resources that are established, analytically demonstrated or assumed with reasonable certainty to be profitable for extraction or production under defined investment assumptions. Classifying a mineral resource as EDR reflects a high degree of certainty as to the size and quality of the resource and its economic viability.

INQUIRIES

For further information about these and related statistics, contact the National Information and Referral Service on 1300 135 070 or Mark Lound on Canberra (02) 6252 6325. The ABS Privacy Policy outlines how the ABS will handle any personal information that you provide to us.

The information on this webpage was last updated by the Government of Australia on 14 April 2016 and downloaded into the TVM system January 25, 2017

|

|

|