|

|

BURGESS POWERPOINT

MIT - Size Matters Workshop

January 2016 ... Organized by John Kiehl

|

MIT - Size Matters Workshop - January 2016 ... 1 - OVERVIEW

https://www.slideshare.net/PeterBurgess2/size-matters1

|

Open external link

|

MIT - Size Matters Workshop - January 2016 ... 2 - KEY CONCEPTS

https://www.slideshare.net/PeterBurgess2/size-matters2

|

Open external link

|

MIT - Size Matters Workshop - January 2016 ... 3 - SYSTEM CYCLES

https://www.slideshare.net/PeterBurgess2/size-matters3

|

Open external link

|

MIT - Size Matters Workshop - January 2016 ... 4 - PERSPECTIVES

https://www.slideshare.net/PeterBurgess2/size-matters4

|

Open external link

|

MIT - Size Matters Workshop - January 2016 ... 5 - IMPACTS

https://www.slideshare.net/PeterBurgess2/size-matters5

|

Open external link

|

|

INCOMPLETE ... EDIT IN PROGRESS

|

1.

File: TVA-p3-00-TVA-for-TBL-1of2-151231.odp

Peter Burgess (c) All rights reserved True Value Accounting for better Triple Bottom Line (TBL) Management PART 1 of 2

2.

CONTEXT This slideset is a Work-in-Progress and will be updated from time to time. It is part of a series that aims to enable better metrics for the complex socio-enviro-economic system that we all live in. Metrics are powerful, but they must be the right metrics.

3.

1. INTRODUCTION AND CONTEXT

4. A COMPLEX SYSTEM

5.

We live in a complex world, that has changed in a massive way over the past 300 years.

6.

This has made it possible for people to have a have a better life in recent times than in the past … longer life … a higher standard of living … a better quality of life.

7.

It is widely recognized that mankind has been a 'toolmaker', and has been able to use 'tools' to become the dominant specie on earth. This was true in the stone age, and it remains true 15 thousand years later.

///////////////////////////////////////////

Published on Jan 20, 2016

SIZE MATTERS-1

1. SIZE MATTERS 1- OVERVIEW

File: TVA-p3-01-SIZE-MATTERS-1-160220.odp

Peter Burgess (c) All rights reserved TRUE VALUE ACCOUNTING

2.

CONTEXT This slideset is a Work-in-Progress and will be updated from time to time.

It is part of a series that aims to enable better metrics for the complex socio-enviro-economic system that we all live in. Metrics are powerful, but they must be the right metrics.

|

3.

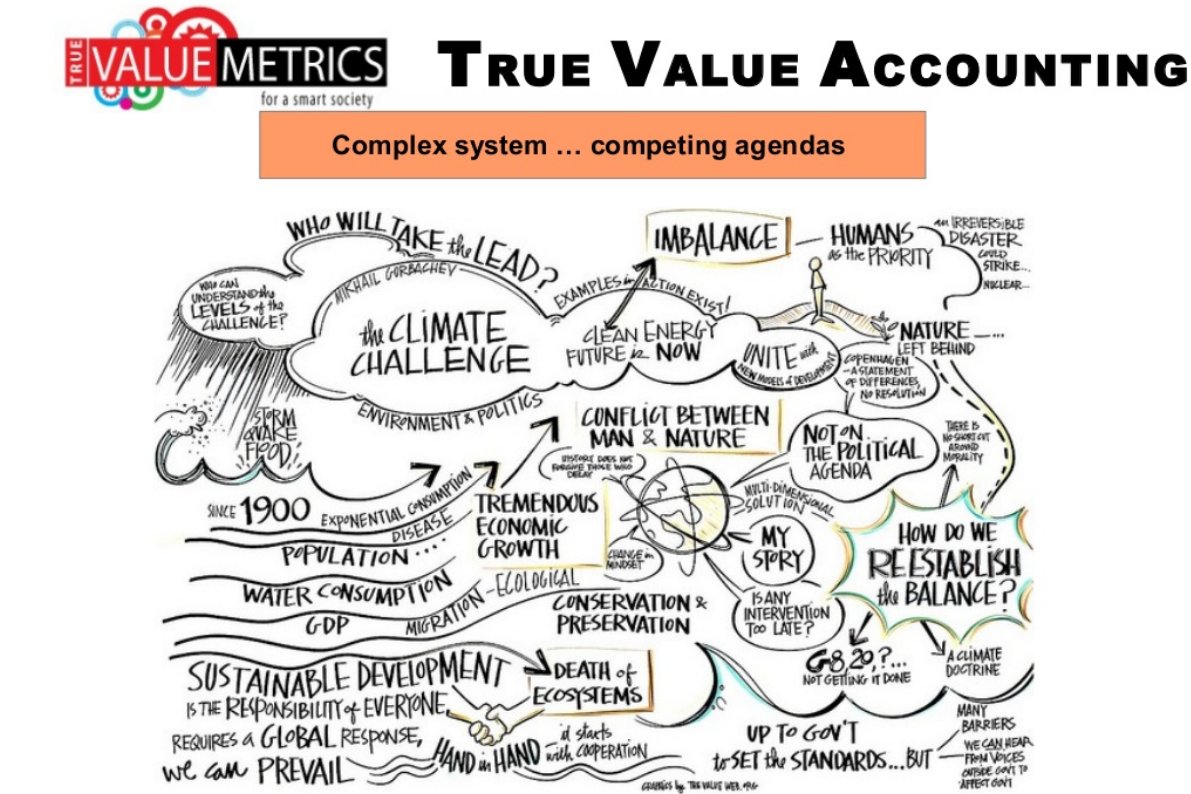

The system is complex …

4.

Complex system … competing agendas

5.

I don't know who drew that image … and have not figured out all its content … but we must figure out the best way to get the best of possible outcomes!

6.

HISTORY … HOW THE THREE SEGMENTS HAVE CHANGED OVER TIME

7.

8.

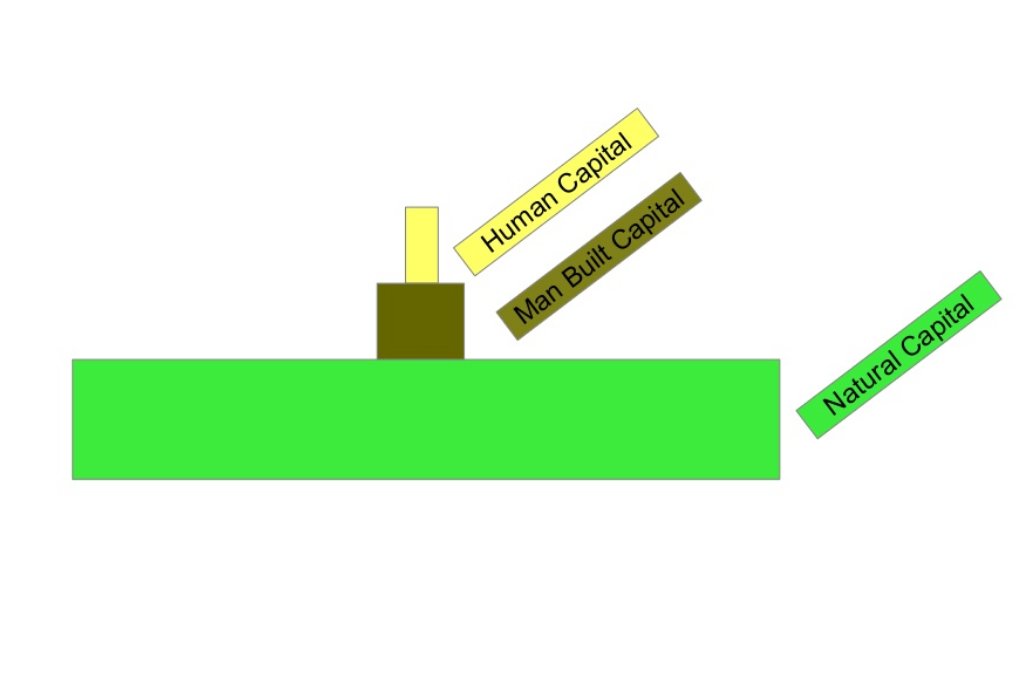

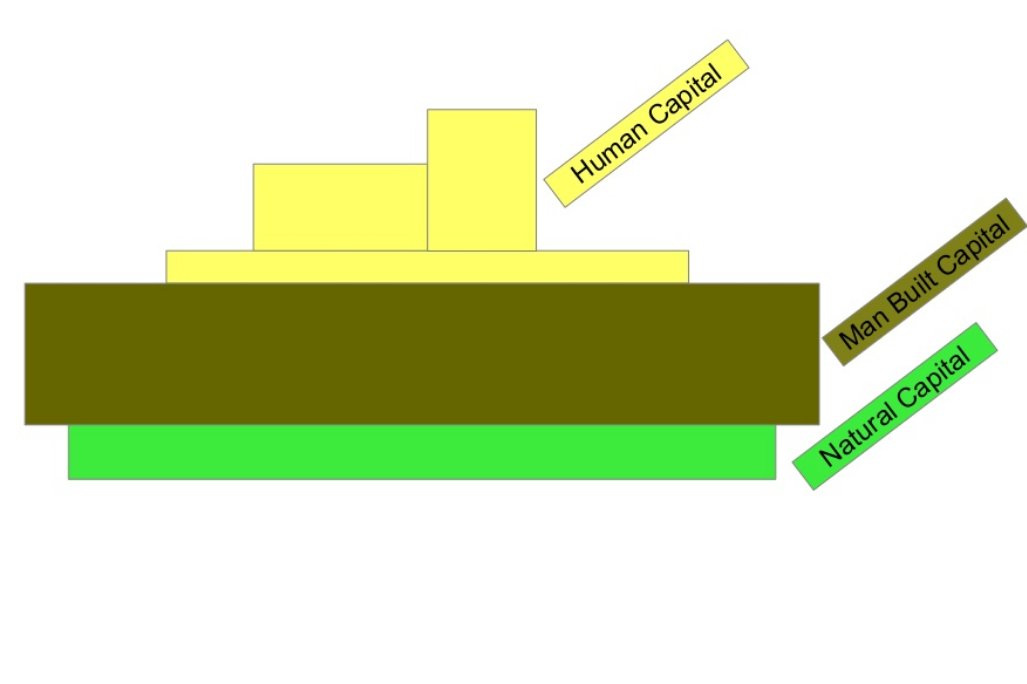

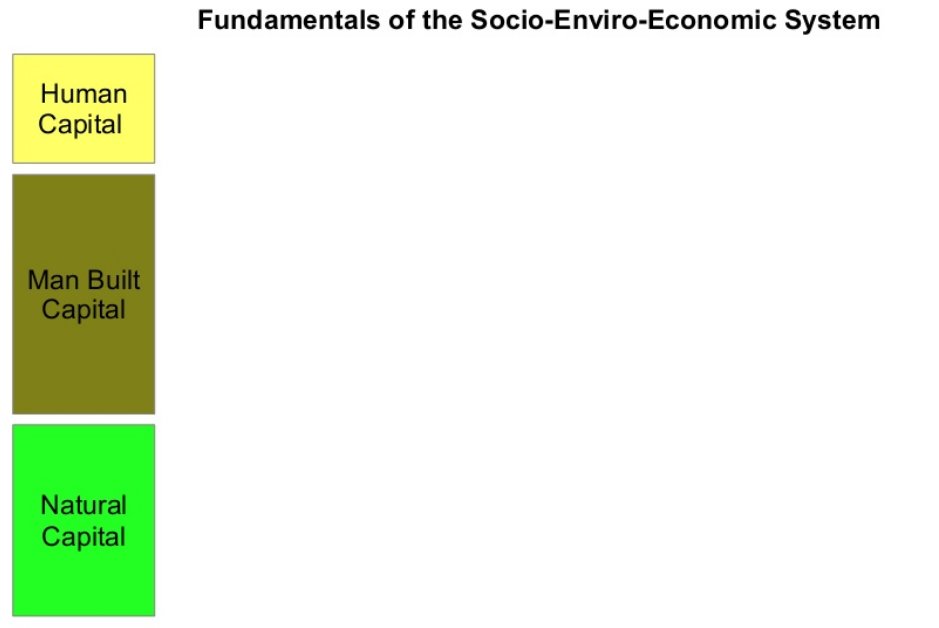

AT THE START

- THERE WERE FEW PEOPLE,

- LITTLE MAN BUILT CAPITAL, AND

- PLENTY OF NATURAL CAPITAL THAT WAS AVAILABLE FOR EXPLOITATION.

9.

10.

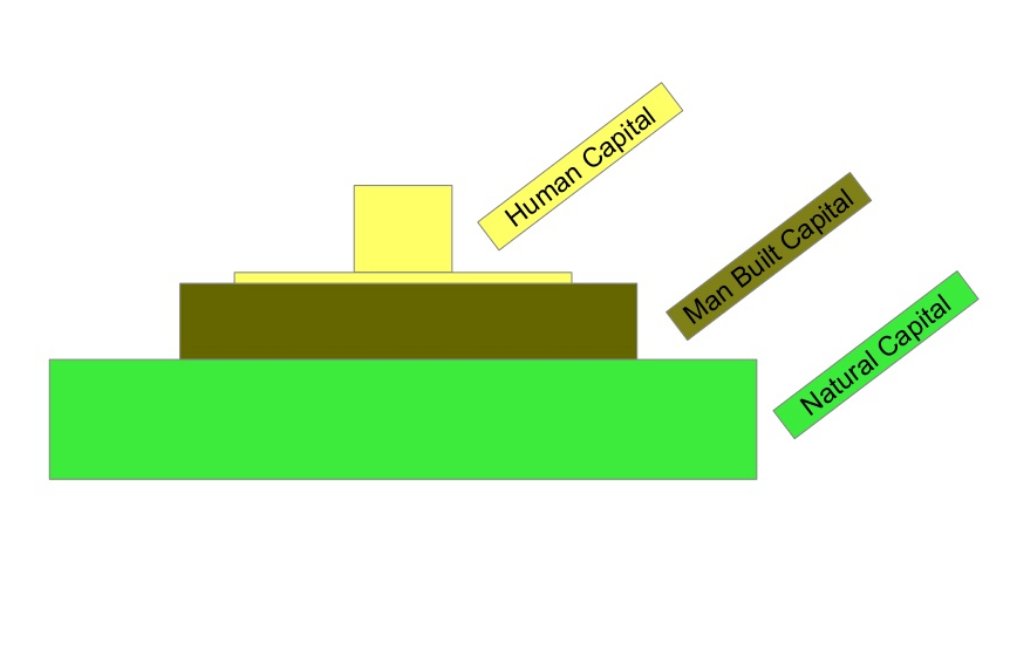

OVER TIME

- MORE PEOPLE,

- MORE MAN BUILT CAPITAL, AND

- EVENTUALLY TOO MUCH PRESSURE ON NATURAL CAPITAL

11.

12.

13.

14.

15.

16.

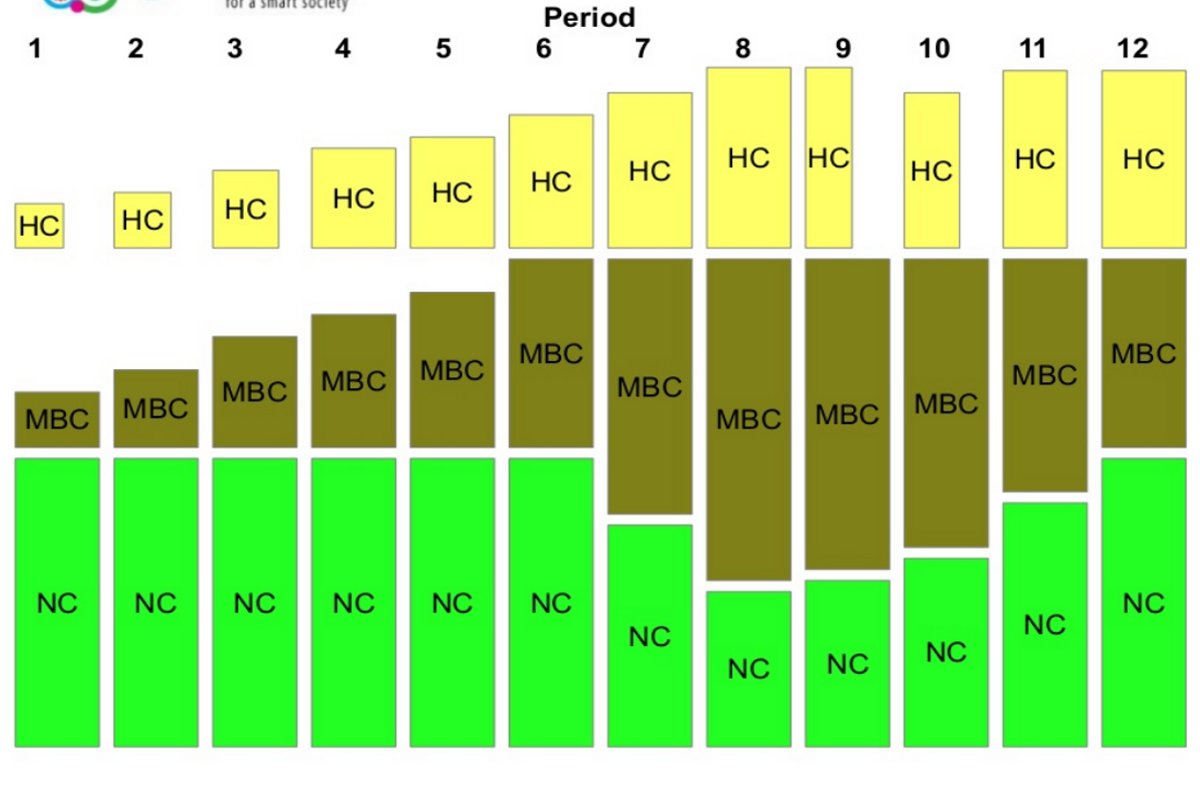

Trajectory to disaster! Over time it looks something like this.

- Period 1-8 past and present

- Period 9-12, a future scenario

17.

18.

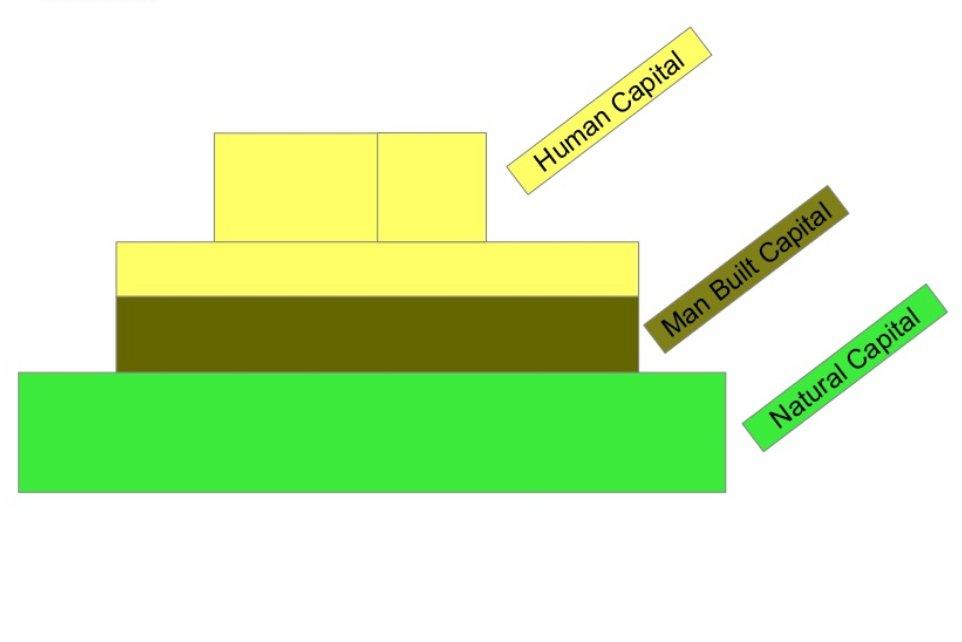

What we need …

19.

20.

- PEOPLE progressing

- MBC* efficient

- PLANET healthy

* Man Built Capital … Man Built Structures and Systems

21.

22.

24.

25.

26.

27.

28.

PROGRESS is Change in STATE during the period. ALL the elements of the BOP and EOP STATES need to be quantified

29.

Any number of activities may take place during a period. They may be extremely complex and interconnected, but PROGRESS is still measured by CHANGE in STATE.

30.

PERFORMANCE is measured by relating PROGRESS achieved with the RESOURCES Consumed. How much is Human Capital increased and how much are Financial, Man Built and Natural Capital diminished

31.

- Financial Capital … virtual masquerading as reality.

- Human Capital … PEOPLE … are complex, because we originated through nature, but our inventions are simple.

- Man Built Capital is so simplistic compared to Natural Capital.

- While in some part amazing, it is very crude compared to what is the norm in Natural Capital.

- In the end it is Natural Capital that is going to determine everything.

- NC is infinitely complex and resilient and will outlast everything Man Built … and People are unlikely to survive in a future mass extinction that is quite certain.

- The source of ALL energy to drive the system

EOP

32.

TVA builds on double entry and the concept of state and flow …

33.

These 3 slides explain the concept of STATE and FLOW … or in accounting terms, the BALANCE SHEET / PROFIT AND LOSS relationship …

34.

STEADY STATE

35.

POSITIVE PROGRESS

36.

DETERIORATION OF STATE

37.

No information about activities is needed in order to measure PROGRESS … only measures about changes in STATE

38.

State, Progress and Performance

- ● State is the Balance Sheet of the entity at a moment in time;

- ● Progress is measured by comparing Balance Sheet changes between the beginning and the end of the period;

- ● Performance is a measurement that relates Progress to the resources consumed.

39.

EFFICIENCY AND EFFECTIVENESS

40.

A fundamental reality … All FINANCIAL WEALTH has been created by human energy together with man built knowledge, structures and systems and exploiting NATURAL CAPITAL in an unsustainable way.

41.

ELEMENTS OF THE SYSTEM by SEGMENT

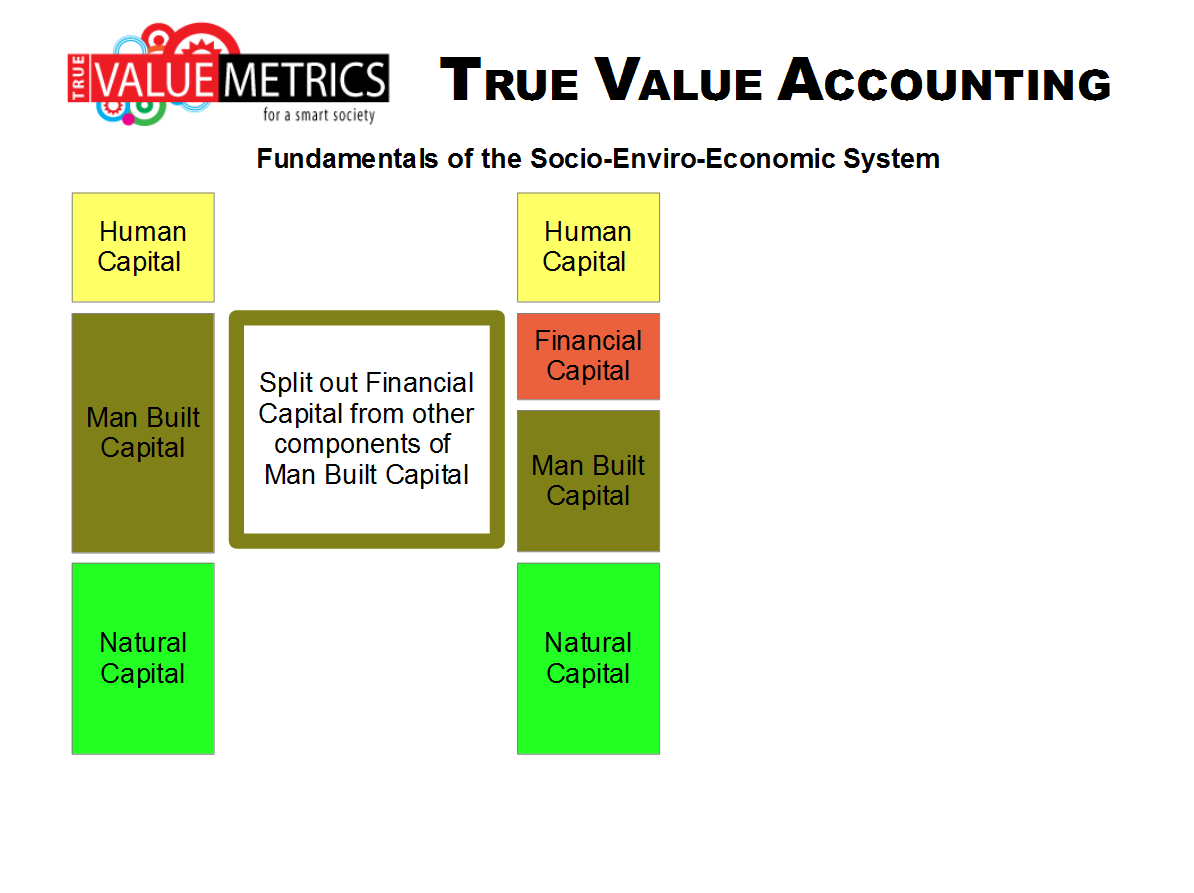

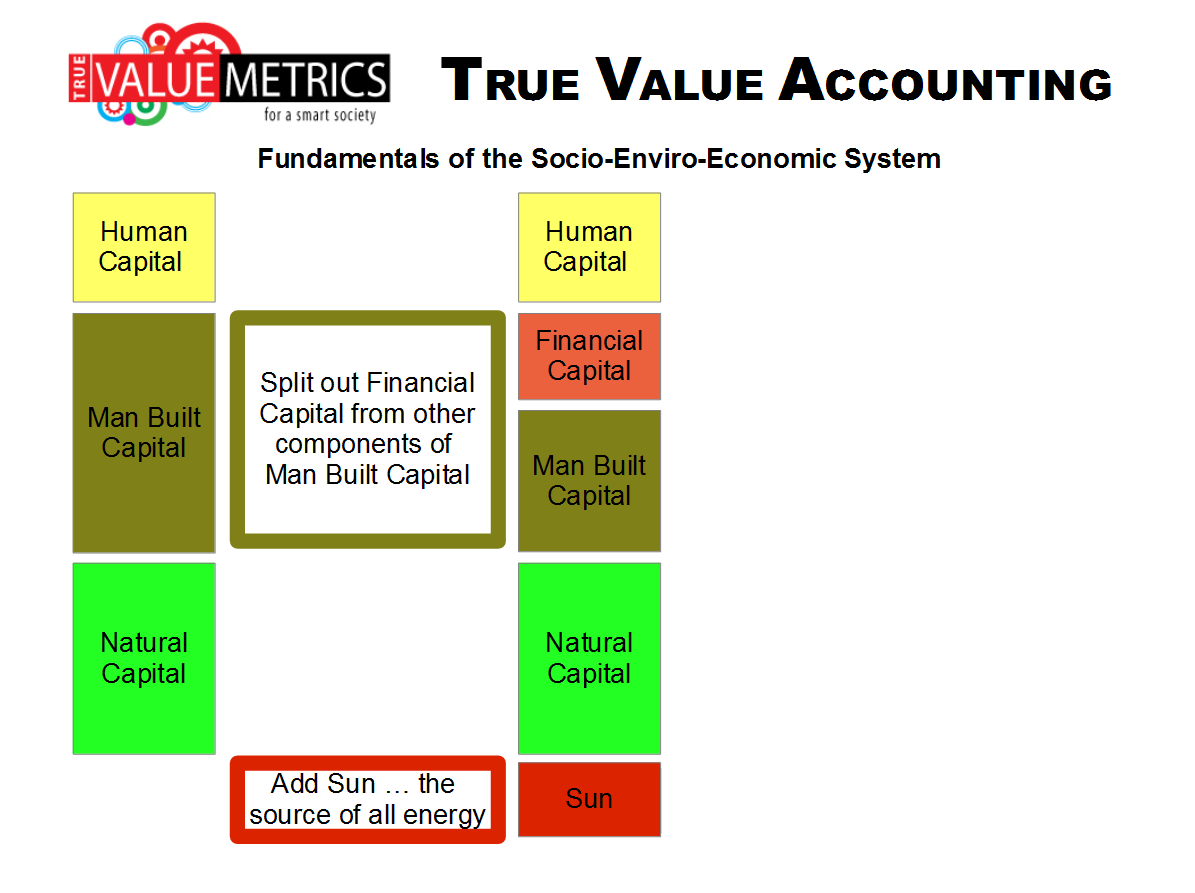

Financial Capital Human Capital Man Built Capital Natural Capital Sun Financial Capital Human Capital Man Built Structures & Systems Natural Capital Money Food Government Nature (life) Sun Nature (life) Capital Market Value Water Laws. Rules Nature (life)Land Shelter Infrastructure WaterClothes Industry Nature (life)Air Health Mining Ecoservices Education EnergySkills Waste Recreation Retail Culture LogisticsReligion Knowledge Technology Security Energy Mobility Profit

42.

Financial Capital Human Capital Man Built Capital Natural Capital Sun

FINANCIAL CAPITAL … virtual masquerading as reality.

As a measure, money is fatally flawed.

The problem is compounded with GDP which ignores almost everything that makes life worth living.

Corporations are high performance in making profit, but issues like social impact and environmental impact are not measured in a meaningful way and therefore Ignored.

43.

Human Capital … PEOPLE … are complex, because we originated through nature, but our inventions are simple.

Food Water Shelter Clothes Energy Health Education Mobility Recreation Culture Religion Recreation Security Skills

44.

Man Built Capital … Structures and Systems Man Built Capital is simple compared to Natural Capital.

It has become very powerful over the past 300 years but at the expense of natural capital and social capital

Government Laws Infrastructure Industry Mining Energy Waste Mobility Logistics Retail Knowledge Technology Financial Capital Human Capital Man Built Capital Natural Capital Sun

45.

NATURAL CAPITAL In the end it is Natural Capital that is going to determine everything.

NC is infinitely complex and resilient and will outlast everything Man Built … and People are unlikely to survive in a future mass extinction that is quite certain.

Nature (life) Millions and millions of miracles, and we only know a small part of it all.

- Land The place where natural systems function, but also where man built processes and structures

- Water Essential to life, man built processes and the natural cycles that sustain nature

- Bio-diversity That has made nature the miracle it is, and fundamental to the functioning of the complex system Air pollution Has impact directly on human health and the functioning of many of the systems of nature

- Eco-system services The myriad of natural recycling mechanisms that serve to keep everything in nature in balance.

- Air GHG Atmospheric processes that regulate climate and the cycles of many critical compounds

46.

SUN The source of ALL the energy that drives the system

ELEMENTS OF THE SYSTEM

47.

Managing in a complex system is a challenge … The best practice it to drive decision making with the best / quickest data about progress and performance and at the most granular level … this is the essence of the TVA data architecture.

48.

To manage change there have to be METRICS for ALL the components of the system.

- ● The next slide is a simplified representation of the State – Flow – State idea for ALL elements of the Socio-Enviro-Economic System

- ● The second slide shows what the conventional money metrics measure … just a tiny part of everything that matters.

49.

STATE - BOP STATE - EOPPERIOD ACTIVITES

50.

STATE - BOP STATE - EOPPERIOD ACTIVITES

51.

Effective metrics will track impact on ALL* the components of the system … * Not just the money based financial metrics

52.

THE BALANCE OF THE SLIDESET IS A RECAP USING IMAGES … This slideset is A WORK-IN-PROGRESS.

It will be upgraded periodically. It is part of a series of more than 100 slidesets.

Navigation to these is available here:

http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=N1-Slidesets-p3

More about the True Value Metrics initiative is at:

http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav

FEEDBACK is welcome.

Please email to Peter Burgess … peterbnyc@gmail.com … with a catchy phrase in the subject line so that it gets attention, and please identify the specific slideset(s) or webpage involved.

53.

THIS SLIDESET IS 1 OF 5

- 1 … OVERVIEW SIZE MATTERS

- 2 … KEY CONCEPTS http://www.slideshare.net/PeterBurgess2/size-matters2

- 3 … SYSTEM CYCLES http://www.slideshare.net/PeterBurgess2/size-matters3

- 4 … PERSPECTIVES http://www.slideshare.net/PeterBurgess2/size-matters4

- 5 … IMPACTS http://www.slideshare.net/PeterBurgess2/size-matters5

54.

Sun BOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPSocio-Enviro-Economic System Hum an Capital Man Built Capital

55.

The next slide shows: PEOPLE MORE THAN 7 BILLION NOW AND GROWING

56.

TRUE VALUE ACCOUNTING

57.

The next slides shows: MAN-BUILT CAPITAL GOVERNMENT, LAW, CITIES, INDUSTRY AND A LOT MORE TRUE VALUE ACCOUNTING

58. TRUE VALUE ACCOUNTING

59. TRUE VALUE ACCOUNTING

60. TRUE VALUE ACCOUNTING

61. TRUE VALUE ACCOUNTING

62. TRUE VALUE ACCOUNTING

63. TRUE VALUE ACCOUNTING

64.

The next slide shows: ENVIRONMENT PLANET EARTH, FAUNA and FLORA TRUE VALUE ACCOUNTING

65. TRUE VALUE ACCOUNTING

66.

The final slide shows: SUN SOURCE OF ALL ENERGY TRUE VALUE ACCOUNTING

67. TRUE VALUE ACCOUNTING

68.

REMINDER This slideset is A WORK-IN-PROGRESS.

It will be upgraded periodically. It is part of a series of more than 100 slidesets. Navigation to these is available here: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=N1-Slidesets-p3 More about the True Value Metrics initiative is at: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav FEEDBACK is welcome. Please email to Peter Burgess … peterbnyc@gmail.com … with a catchy phrase in the subject line so that it gets attention, and please identify the specific slideset(s) or webpage involved. TRUE VALUE ACCOUNTING

69.

THANK YOU

Some links and contact information: Email Peter Burgess … peterbnyc@gmail.com Peter Burgess LinkedIn profile https://www.linkedin.com/in/peterburgess1 Link to TrueValueMetrics.org website http://www.truevaluemetrics.org/ Link to navigation to other resources: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav#1 TRUE VALUE ACCOUNTING

///////////////////////////////////////////////////////////////////////

SIZE MATTERS-2

393 views

Share Like Download ...

Peter Burgess

Peter Burgess, Founder/CEO at TrueValueMetrics developing Multi Dimension Impact Accounting

Follow

Published on Jan 20, 2016

SIZE MATTERS 2 ... KEY CONCEPTS

A workshop at MIT to link mathematics with

...

Published in: Data & Analytics

0 Comments

0 Likes

Statistics

Notes

no profile picture user

Share your thoughts…

Post

Be the first to comment

SIZE MATTERS-2

1. SIZE MATTERS 2 - KEY CONCEPTS File:

TVA-p3-01-SIZE-MATTERS-2-160220.odp

Peter Burgess (c) All rights reserved TRUE VALUE ACCOUNTING

2. CONTEXT

This slideset is a Work-in-Progress and will be updated from time to time. It is part of a series that aims to enable better metrics for the complex socio-enviro-economic system that we all live in. Metrics are powerful, but they must be the right metrics. TRUE VALUE ACCOUNTING

3. Key Concepts from Accountancy:

● Double Entry Accounting;

● State, Process and Flow;

● State, Progress and Performance;

● Cost, Price and Value;

● Quantification;

● Standard Value;

● Data at the Center;

● Feedback;

● Reporting Boundaries;

● Consolidation Rules.

4.

Double entry accountancy is surprisingly respectful of the key characteristics of engineering thermodynamics, but this is only applied to account for money based transactions and impact on business performance. TRUE VALUE ACCOUNTING

5.

Conventional accounting ignores impact on society and environment. Everything beyond the business and outside the reporting envelope is ignored no matter how important. The idea of 'entropy' is not taken into account in the way metrics work for the system. TRUE VALUE ACCOUNTING

6.

It is a fundamental reality that all WEALTH measured in money has been created by human energy together with man built knowledge, structures and systems and exploiting NATURAL CAPITAL … and in an unsustainable way. TRUE VALUE ACCOUNTING

7.

The purpose of data is to enable good decisions to be made in a timely manner and with high reliability. Data must be low cost. Data must be relevant in order to be useful for decision makers. The best decisions are made at a low level in the system hierarchy.

8. Double Entry Accounting

● Double Entry is the core strength of a good accounting system; ● Every money transaction impacts two accounts; and the system as a whole is always in balance; ● Enables analysis of State, Process and Flow The next three slides show how ACTIVITY or process and flow changes STATE

9. STEADY STATE

10. POSITIVE PROGRESS

11. DETERIORATION OF STATE

12.

No information about ACTIVITIES is needed in order to measure PROGRESS … only information about changes in STATE

13. Data at the Center

● Used to plan ● Used to organize ● Used to implement ● Used to monitor progress ● Used to monitor cost effectiveness ● Used to plan follow up next steps

14.

15. State, Progress and Performance

● State is the Balance Sheet of the entity at a moment in time; ● Progress may be measured by comparing the Balance Sheet changes between the beginning and the end of the period; ● Performance is a measurement that relates the Progress to the resources consumed.

16. EFFICIENCY AND EFFECTIVENESS

17. Cost, Price and Value

● There should be clarity about what is cost and what is price; ● A buy/sell transaction takes place at a price; ● The buy price becomes the buyer's cost; ● There is a lot of data about price, but relatively little accessible data about cost; ● Value is a very important idea, but quantified data about value is missing; ● Money cost, price and value ignore all about impact on people and planet.

18. TRUE VALUE ACCOUNTING

The money cost of the resources used to make the productCost Price Value The money amount that exchanged when the product is bought or sold A notional amount that is ascribed to the product by an owner or user

19. Profit, ValueAdd and Value Destruction

Profit is Price minus Cost. Valueadd and value destruction are computed from Value and Cost. Understanding valueadd and value destruction will be a game changer. These are much more relevant concepts than the simplistic money profit metric.

20.

21. IMPACT ACCOUNTING

Moving from Financial to Impact Accounting

STATE BOP … ACTIVITY ACCOUNTING … STATE EOP TRUE VALUE ACCOUNTING

22. Moving from Financial to Impact Accounting

STATE BOP … ACTIVITY ACCOUNTING … STATE EOP ● Financial accounting; ● P&L and Balance Sheets (BOP and EOP); ● Financial accounting plus GOOD impacts; ● Financial accounting minus BAD impacts; ● Financial accounting with BOTH impacts; ● Bringing in IMPACTS on externalities; ● Expanding the REPORTING ENVELOPE; ● Accounting for IMPACT on ALL capitals. TRUE VALUE ACCOUNTING

23. FINANCIAL ACCOUNTS

Financial Accounts describe Economic Activity REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit

24. FINANCIAL ACCOUNTS OF AN ENTERPRISE

Financial Accounts describe Economic Activity REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit Cash Current Assets Fixed Assets Intangible Assets TOTAL ASSETS Current Liabilities Long Term Debt Owners' Equity Cash Current Assets Fixed Assets Intangible Assets TOTAL ASSETS Current Liabilities Long Term Debt Owners' Equity Balance Sheet BOP Balance Sheet EOP TRUE VALUE ACCOUNTING

25. FINANCIAL ACCOUNTS ADD positive impact not accounted for

REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit

REVENUES Products Sold X Price VALUE to buyer Equals HUMAN CAPITAL ADD Wages and benefits What value to employee? Pro-good expenditures What value to society? Taxation What value to society? POSITIVE IMPACT NOT ACCOUNTED FOR

26.

FINANCIAL ACCOUNTS DEDUCT negative impact not accounted for REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit For products and energy bought and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation Negative impact

27. FINANCIAL ACCOUNTS ACCOUNTING FOR EVERYTHING

REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit REVENUES Products Sold X Price VALUE to buyer Equals HUMAN CAPITAL ADD Wages and benefits What value to employee? Pro-good expenditures What value to society? Taxation What value to society? For products and energy bought and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation POSITIVE IMPACT NOT ACCOUNTED FOR Negative impact

28.

Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes TRUE VALUE ACCOUNTING

29.

Financial Accounts describe Financial Impact Impact Accounts reflect Externalities Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes TRUE VALUE ACCOUNTING Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes

30.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun Financial Accounts describe Financial Impact Impact Accounts reflect Externalities Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes TRUE VALUE ACCOUNTING Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes

31.

Ignoring Externalities is Absurd ... Conventional accounting enables the ignoring of externalities. With no money transaction there is nothing … which is patently absurd … but is the norm and has been for decades. TRUE VALUE ACCOUNTING, integrated impact accounting addresses this critical dysfunction.

32. QUANTIFICATION

33. Quantification

Putting numbers on measures is a vital step in enabling management to make good decisions:

● Money is used to measure profit and much to do with financial capital.

● A measure is needed for everything to do with human life and quality of life … human capital

● Other measures are needed for :

● The Carbon Cycle;

● The Water Cycle;

● Land use (including ecosystem services);

● Various Nutrient Cycles.

● Not to mention better accounting for risk.

34. The role of monetization

Monetization is fatally flawed as a method for measurement. An exchange transaction … a market … gives a result based more than anything else on supply and demand. It is a 'result' and not a 'measure'.

35. Standard Value

Cost accounting is often based on a framework of standard costs. Impact accounting can be based on a similar system of standards. The standard is the norm. Variations from the norm are identified and used to prioritize action plans to improve performance

36. A COMPLEX SYSTEM

The system is complex … a host of different agendas, goals, and behaviors …

37.

Complex system … competing agendas

38. My version of amazing complexity …

● Global North/Global South/Community

● Big Organizations - National and International / Small communities

● Elements of Society: National level and community

39.

40.

41.

42. FEEDBACK

Feedback design is key to rapid change … everyone should have easy quick data that helps the making of better decisions

43.

● Feedback is best when it is fast and very focused on practical actionable response

● In this example feedback happens in the small community BEFORE the data reaches city, state, national and big data systems at the international level.

44.

45.

The next slides STATE BOP … ACTIVITY … STATE EOP How to apply the MDIA core concepts to the supply chain:

● First thinking it terms of money profit

● Secondly adding in the impact on people, society and the environment.

46. Sun

FINANCIAL ACCOUNTS Economic Activity … Process Accounts REVENUES Products Sold X Price Products Bought X Price BOP EOP Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit File: MDIA-Framework-004-150411-WIP.odp Peter Burgess (c) All rights reserved Sun Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun SunSun Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun

47. MBSS Natural Capital Human Capital PRODUCT

… the SUPPLY CHAIN IMPACT ACCOUNTING ADJUSTMENTS Zero to start Costs this stage Profit this stage Price this stage FINANCIAL ACCOUNTS Zero to start Costs this stage Profit this stage Price Stage 1 FINANCIAL ACCOUNTS EACH STEP OF THE SUPPLY CHAIN Cost = Price stage 1 Costs Stage 2 Profit Stage 2 Impact Stage 1 Impact Stage 1 Impact Stage 1 Cum Costs Cum Profit Price Stage 2 Impact Stage 2 Impact Stage 2 Impact Stage 2 Cum Impact Cum Impact Cum Impact Cost = Price stage 2 Costs Stage 3 Profit Stage 3 Cum Costs Cum Profit Price Stage 3 Impact Stage 3 Impact Stage 3 Impact Stage 3 Cum Impact Cum Impact Cum Impact Financial Dimension File: MDIA-Framework-004-150411-WIP.odp Peter Burgess (c) All rights reserved

48. MBSS Natural Capital Human Capital PLACE

… Where people live and work … where impact can be seen IMPACT ACCOUNTING ADJUSTMENTS Zero to start Costs this stage Profit this stage Price this stage FINANCIAL ACCOUNTS Zero to start Costs this stage Profit this stage Price Stage 1 FINANCIAL ACCOUNTS EACH STEP OF THE SUPPLY CHAIN

Impact Stage 1 Impact Stage 1 Impact Stage 1 Financial Dimension File: MDIA-Framework-004-150411-WIP.odp

Peter Burgess (c) All rights reserved

49. Sun

Small decisions by people make all the difference

BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun

50. Sun Small decisions by people make all the difference

BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun

51. Sun Small decisions by people make all the difference

BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun Product Place Supply Chain Process Organization Enabling environment Society

52. Sun Small decisions by people make all the difference

BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun

53. Sun Small decisions by people make all the difference

BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun

54. Sun External Resources Create Impact Value

Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun

55. THIS SLIDESET IS 2 OF 5 SIZE MATTERS

1 … OVERVIEW http://www.slideshare.net/PeterBurgess2/size-matters1 SIZE MATTERS 2 … KEY CONCEPTS SIZE MATTERS 3 … SYSTEM CYCLES http://www.slideshare.net/PeterBurgess2/size-matters3 SIZE MATTERS 4 … PERSPECTIVES http://www.slideshare.net/PeterBurgess2/size-matters4 SIZE MATTERS 5 … IMPACTS http://www.slideshare.net/PeterBurgess2/size-matters5

56. REMINDER This slideset is A WORK-IN-PROGRESS.

It will be upgraded periodically. It is part of a series of more than 100 slidesets. Navigation to these is available here: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=N1-Slidesets-p3 More about the True Value Metrics initiative is at: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav FEEDBACK is welcome. Please email to Peter Burgess … peterbnyc@gmail.com … with a catchy phrase in the subject line so that it gets attention, and please identify the specific slideset(s) or webpage involved.

57. THANK YOU

Some links and contact information: Email Peter Burgess … peterbnyc@gmail.com Peter Burgess LinkedIn profile https://www.linkedin.com/in/peterburgess1 Link to TrueValueMetrics.org website http://www.truevaluemetrics.org/ Link to navigation to other resources: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav#1

https://www.slideshare.net/PeterBurgess2/size-matters2

/////////////////////////////////////////////////////////////////////

SIZE MATTERS-3

167 views

Share Like Download ...

Peter Burgess

Peter Burgess, Founder/CEO at TrueValueMetrics developing Multi Dimension Impact Accounting

Follow

Published on Jan 24, 2016

SIZE MATTER 3 ... SYSTEM CYCLES

A workshop at MIT to link mathematics with

...

Published in: Data & Analytics

0 Comments

0 Likes

Statistics

Notes

no profile picture user

Share your thoughts…

Post

Be the first to comment

SIZE MATTERS-3

1. SIZE MATTERS 3-

SYSTEM CYCLES File: TVA-p3-01-SIZE-MATTERS-3-160220.odp Peter Burgess (c) All rights reserved TRUE VALUE ACCOUNTING

2. CONTEXT

This slideset is a Work-in-Progress and will be updated from time to time. It is part of a series that aims to enable better metrics for the complex socio-enviro-economic system that we all live in. Metrics are powerful, but they must be the right metrics.

3.

The system is complex …

4.

Complex system … competing agendas

5. Managing in a complex system is a challenge …

The best practice it to drive decision making with the best / quickest data about progress and performance and at the most granular level … this is the essence of the TVA data architecture.

6. MULTI DIMENSION IMPACT ACCOUNTING CARBON CYCLE

7. MULTI DIMENSION IMPACT ACCOUNTING

University-of-Michigan-Carbon-Cycle-Lecture-Notes A very readable paper about the CARBON CYCLE from the University of Michigan …

8.

CARBON … an enormously important scientific element. … and a critical link between chemistry and biology

9.

The burning of CARBON produces carbon dioxide, a colorless gas that changes the heat transfer properties of the atmosphere. The chemical formula for carbon dioxide is CO2

10.

CO2 is a Greenhouse Gas (GHG) … an important causal factor in global warming.

11.

The following slides show various depictions of the CO2 dimension of the CARBON CYCLE MULTI DIMENSION IMPACT ACCOUNTING

12.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOP

13.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPCARBON CYCLE

14.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPCARBON RESERVOIRS AND FLUXES

15.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPCARBON CYCLE – CARBON STORES

16.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPCARBON SINK

17.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPTEMPERATURE HISTORY

18.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPTEMPERATURE HISTORY

19.

LOCATION Billion tons carbon Rocks Oceans Soils Atmosphere (at 360ppm) Vegetation 1015 g = 1 billion tons = 1 gigaton = 1 Pedagram MULTI DIMENSION IMPACT ACCOUNTING 65,000,000 39,000 1,580 750 6

10 STOCKS OF CARBON

20.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPCARBON … STOCKS AND FLOWS

21.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPCARBON DIOXIDE CONCENTRATIONS

22.

In addition to CARBON DIOXIDE, there is also METHANE with the formula CH4 METHANE is a far more potent greenhouse gas (GHG) than CO2 by a factor of more than twenty.

23.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPMETHANE CYCLE

24.

NITROGEN CYCLE

25.

NITROGEN plays an important role in the cycle of nature …

26.

NITROGEN is an element in many compounds including:

● Ammonia (NH4);

● Nitrous dioxide (NO2);

● Nitrates;

● Nitrites;

● etc.

27.

Many natural processes involving plants, bacteria and fungi convert these various compounds to build balance in nature …

28.

NITROGEN plays an important role in the cycle of nature, but its heavy use in modern industry and agriculture has disrupted the equilibrium of the natural cycle MULTI DIMENSION IMPACT ACCOUNTING

29.

There are many ways to represent the NITROGEN CYCLE …

30.

Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun EOP Financial Capital Human Capital Man Built Capital Natural Capital Nitrogen Cycle

31.

Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun EOP Financial Capital Human Capital Man Built Capital Natural Capital Nitrogen CycleNitrogen Cycle

32.

Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun EOP Financial Capital Human Capital Man Built Capital Natural Capital Nitrogen Cycle

33.

Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun EOP Financial Capital Human Capital Man Built Capital Natural Capital Nitrogen Cycle

34.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun Nitrogen Cycle

35.

Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun Financial Capital Human Capital Man Built Capital Natural Capital EOPNitrogen Cycle

36.

NITROGEN is important … but the balance of this system is outside the 'planetary bounds' according to the scientists … MULTI DIMENSION IMPACT ACCOUNTING

37.

Sun BOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun EOPPlanetary Boundaries Image credit: Steffen et al. Science (2015). Journal Science / AAAS

38.

WATER CYCLE

39.

WATER WATER FLOW SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun

40.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun

41.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun

42.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun

43.

Values in 1000 cubic km/yr SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun

44.

Values in 1000 cubic km/yr SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun Nitrogen cycle

45.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun

46.

Link to: University-of-Michigan ... The-Global-Water-and-Nitrogen-Cycles WATER CYCLE A very readable paper about the WATER CYCLE is this from the University of Michigan …

47.

The STOCK of WATER Cubic Kilometers Rocks (not usable) Oceans (97.4% of usable water) Ice Groundwater Lakes and Rivers Atmosphere (vapor) 150,000,000 1,350,000,000 27,500,000 15,300,000 25,000 13,000

48.

SunSun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun A huge amount of water … but most is not potable

49.

IF ½ OF THE ICE MELTED, this would result in a 26.2 metre rise in sea level … about 86 feet! Cubic Kilometers Total ice 50% of ice = Square kilometers Surface area of the oceans Metres Sea level rise (average) MULTI DIMENSION IMPACT ACCOUNTING 27,500,000 13,750,000 360,000,000 26.2

50.

THIS SLIDESET IS 3 OF 5

SIZE MATTERS 1 … OVERVIEW http://www.slideshare.net/PeterBurgess2/size-matters1

SIZE MATTERS 2 … KEY CONCEPTS http://www.slideshare.net/PeterBurgess2/size-matters2

SIZE MATTERS 3 … SYSTEM CYCLES

SIZE MATTERS 4 … PERSPECTIVES http://www.slideshare.net/PeterBurgess2/size-matters4

SIZE MATTERS 5 … IMPACTS http://www.slideshare.net/PeterBurgess2/size-matters5

51.

REMINDER This slideset is A WORK-IN-PROGRESS. It will be upgraded periodically. It is part of a series of more than 100 slidesets. Navigation to these is available here: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=N1-Slidesets-p3 More about the True Value Metrics initiative is at: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav FEEDBACK is welcome. Please email to Peter Burgess … peterbnyc@gmail.com … with a catchy phrase in the subject line so that it gets attention, and please identify the specific slideset(s) or webpage involved. TRUE VALUE ACCOUNTING

52.

THANK YOU Some links and contact information: Email Peter Burgess … peterbnyc@gmail.com Peter Burgess LinkedIn profile https://www.linkedin.com/in/peterburgess1 Link to TrueValueMetrics.org website http://www.truevaluemetrics.org/ Link to navigation to other resources: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav#1 TRUE VALUE ACCOUNTING

https://www.slideshare.net/PeterBurgess2/size-matters3

///////////////////////////////////////////////////////////////

SIZE MATTERS-4

204 views

Share Like Download ...

Peter Burgess

Peter Burgess, Founder/CEO at TrueValueMetrics developing Multi Dimension Impact Accounting

Follow

Published on Jan 24, 2016

SIZE MATTERS 4 ... PERSPECTIVES

A workshop at MIT to link mathematics with

...

Published in: Data & Analytics

0 Comments

0 Likes

Statistics

Notes

no profile picture user

Share your thoughts…

Post

Be the first to comment

SIZE MATTERS-4

1.

TVA-p3-01-SIZE MATTERS-4-160220.odp Peter Burgess (c) All rights reserved

SIZE MATTERS 4- PERSPECTIVES

2.

TVA-p3-01-SIZE MATTERS-4-160124.odp Peter Burgess (c) All rights reserved PERSPECTIVESMEASURING PROGRESS AND PERFORMANCE OF THE SOCIO-ENVIO-ECONOMIC SYSTEM FROM EVERY POINT OF VIEW

3.

CONTEXT This slideset is a Work-in-Progress and will be updated from time to time. It is part of a series that aims to enable better metrics for the complex socio-enviro-economic system that we all live in. Metrics are powerful, but they must be the right metrics.

4.

PERSPECTIVE ... An object looks very different depending on the position of the observer. But it is the same object nevertheless.

5.

6.

In the complex global socio-enviro- economic system, multiple PERSPECTIVES are essential ... One perspective … that of the business organization … is not enough, but that is really all there is.

7.

Multiple PERSPECTIVES are essential, that of:

● the ORGANIZATION;

● PEOPLE;

● PROCESS;

● PRODUCT;

● PLACE;

● Natural Capital at the local level; and,

● Natural Capital at the global level.

8.

TRIPLE BOTTOM LINE (TBL) The idea of the Triple Bottom Line … PROFIT, PEOPLE and PLANET has been around since the 1990s*. This is good, but while it broadens the scope of the metrics it remains focused on the performance and perspective of the ORGANIZATION. MULTI DIMENSION IMPACT ACCOUNTING * When it was first described by John Elkington

9.

THE CHALLENGE The challenge is to have a data system that is meaningful from every perspective of the socio-enviro-economic-system. Hence, the need for a data framework that has Multi Dimensions and enables Multi Perspectives

10.

SOLUTION: True Value Accounting TVA uses concepts from conventional double entry accounting where there are both Balance Sheet and Profit and Loss Accounts. The building block for TVA is similar … State1 → Flow → Process → Flow → State2 … a scheme that can be applied to every economic activity in any setting anywhere. MULTI DIMENSION IMPACT ACCOUNTING

11.

This TVA building block enables:

● Aggregation to enable summary reporting; and

● Drill down to activities that are relevant at every subsidiary level down to the individual level.

12.

SO … How do we go from an economy where there is a singular focus on PROFIT to something that embraces ALL the dimensions of the global complex socio-enviro-economic system? How do these all come together as a single coherent system?

13.

SO … What is the PEOPLE perspective? What is the ORGANIZATION perspective? What is the PRODUCT perspective? What is the PROCESS perspective? What is the PLACE perspective? What impacts on NATURAL CAPITAL? How do these all come together as a single coherent system?

14.

How must the components of Man Built Capital (MBC) be changed to get best possible results? How can people in organizations collectively make better decisions? How can people buying products make better decisions?

15.

Part of the answer is BETTER METRICS

16.

TVA tracks impact on ALL* the components of the system … * Not just the money based financial metrics

17.

Financial Capital Human Capital Man Built Capital Natural Capital Sun Financial Capital Human Capital Man Built Capital Natural Capital MoneyFood Government Nature (life) Sun Nature (life) Capital Market Value Water Laws. Rules Nature (life)Land Shelter Infrastructure WaterClothes Industry Nature (life)Air Health Mining Ecoservices Education EnergySkills Waste Recreation Retail Culture LogisticsReligion Knowledge Technology Security Energy Mobility Profit More Elements of the MDIA Framework

18.

Note that FINANCIAL CAPITAL has been separated out from the other parts of the MBC segment Note also the addition of SUN to enable metrics about renewables MULTI DIMENSION IMPACT ACCOUNTING

19.

Financial Capital Human Capital Man Built Capital Natural Capital SunSun Financial Capital Human Capital Man Built Capital Natural Capital SunSunSun Man Built Capital Natural Capital Sun Human Capital Add Sun … the source of all energy Split out Financial Capital from other components of Man Built Capital Reorder because Financial Capital metrics exist Making MDIA coherent with Socio-Enviro-Economic System Human Capital

20.

Things change over time … STATE* changes * Think the 'State of the Union' message that the President of the United States delivers each year to Congress

21.

There must be clarity about STATE and FLOW … or in accounting terms, the BALANCE SHEET and the PROFIT AND LOSS ACCOUNT. PROGRESS is change in STATE …

22.

POSITIVE PROGRESS

23.

Integrate this idea into the multi capital TVA framework …

24.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun Economic Activity or Process Transformation --->

25.

Practically every organization on the planet has financial accounts that record money transactions and report money related performance …

26.

Financial accounts describe economic activity in money or financial terms while completely ignoring impact on everything else

27.

FINANCIAL P&L ACCOUNT Financial Accounts describe Economic Activity REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation PROFIT COSTS

28.

The next slides show how IMPACT must be incorporated into the data architecture …

29.

ADD positive impact not accounted for REVENUES Products Sold X Price VALUE to buyer Equals HUMAN CAPITAL ADD Wages and benefits What value to employee? Pro-good expenditures What value to society? Taxation What value to society? POSITIVE IMPACT NOT ACCOUNTED FOR FINANCIAL P&L ACCOUNT REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation PROFIT COSTS

30.

DEDUCT negative impact not accounted for For products and energy bought and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation Negative impact FINANCIAL P&L ACCOUNT REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation PROFIT COSTS

31.

ACCOUNTING FOR EVERYTHING REVENUES Products Sold X Price VALUE to buyer Equals HUMAN CAPITAL ADD Wages and benefits What value to employee? Pro-good expenditures What value to society? Taxation What value to society? For products and energy bought and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation POSITIVE IMPACT NOT ACCOUNTED FOR Negative impact FINANCIAL P&L ACCOUNT REVENUES Products Solt and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation Negative impact FINANCIAL P&L ACCOUNT REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation PROFIT COSTS

31.

ACCOUNTING FOR EVERYTHING REVENUES Products Sold X Price VALUE to buyer Equals HUMAN CAPITAL ADD Wages and benefits What value to employee? Pro-good expenditures What value to society? Taxation What value to society? For products and energy bought and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation POSITIVE IMPACT NOT ACCOUNTED FOR Negative impact FINANCIAL P&L ACCOUNT REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation PROFIT COSTS

32.

Because of the way double entry accounting works … the operating accounts (P&L) for an economic activity or process result in changes to the Balance Sheet of the entity … MULTI DIMENSION IMPACT ACCOUNTING

33.

Financial Accounts describe Economic Activity Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP

34.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun Financial Accounts describe Economic Activity Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP

35.

Economic operations also have IMPACTS on human capital (people), on man built capital (MBC) and natural capital (environment / planet) … but these are outside the 'reporting boundary' for the entity.

36.

Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes

37.

Integrated accounting for IMPACT requires the reporting boundary to extend to all the extremities of the system in one coherent system as shown in this next graphic …

38.

Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes

39.

A world with just one economic activity will look like this …

40.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes

41.

Or like this …

42.

Sun Every single PROCESS has IMPACT on EVERYTHINGBOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun

43.

Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes Where this ... represents this ...

44.

The ORGANIZATION perspective ... The operations of an organization are the aggregation of all the economic activities or operations of the organization. For money accounting there are established rules how this consolidation is done. Similar rules are needed for the aggregation of impact for the organization.

45.

A world with no economic activity is represented by this …

46.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun

47.

SO … the ORGANIZATION is represented in this way …

48.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun ORGANIZATION with one operation

49.

An organization with many operations looks like this …

50.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun ORGANIZATION with many operations

51.

And a PRODUCT aggregates in a very similar way …

52.

Sun PRODUCT made by one PROCESSBOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun

53.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun PRODUCT PRODUCT … the result of a SUPPLY CHAIN … with series of PROCESSES

54.

The money accounting presentation of the SUPPLY CHAIN may have this form …

55.

MBC Natural Capital Human Capital PRODUCT … the SUPPLY CHAIN EXTERNALITIES IGNORED Zero to start Costs this stage Profit this stage Price this stage Zero to start Costs this stage Profit this stage Price Stage 1 FINANCIAL ACCOUNTS EACH STEP OF THE SUPPLY CHAIN Cost = Price stage 1 Costs Stage 2 Profit Stage 2 Cum Costs Cum Profit Price Stage 2 Cost = Price stage 2 Costs Stage 3 Profit Stage 3 Cum Costs Cum Profit Price Stage 3 Financial Dimension ETC... The supply chain optimizes through the interaction of price for the buyer and profit for the seller … impact on externalities is not part of the equation.

56.

… and the IMPACT ACCOUNTING for the SUPPLY CHAIN needs to look something like this …

57.

MBSS Natural Capital Human Capital PRODUCT … the SUPPLY CHAIN ADJUSTMENTS TO REFLECT IMPACT (EXTERNALITIES) Zero to start Costs this stage Profit this stage Price this stage Zero to start Costs this stage Profit this stage Price Stage 1 FINANCIAL ACCOUNTS EACH STEP OF THE SUPPLY CHAIN Cost = Price stage 1 Costs Stage 2 Profit Stage 2 Impact Stage 1 Impact Stage 1 Impact Stage 1 Cum Costs Cum Profit Price Stage 2 Impact Stage 2 Impact Stage 2 Impact Stage 2 Cum Impact Cum Impact Cum Impact Cost = Price stage 2 Costs Stage 3 Profit Stage 3 Cum Costs Cum Profit Price Stage 3 Impact Stage 3 Impact Stage 3 Impact Stage 3 Cum Impact Cum Impact Cum Impact Financial Dimension

58.

The progress and performance of a PLACE is also a result of the aggregation of many economic activities …

59.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun PLACE with many economic activities

60.

Quality of Life for PEOPLE is determined by: Everything that is in the PLACE. The availability and flow of PRODUCTS. Access to OPPORTUNITIES (typically associated with an ORGANIZATION and availability jobs).

61.

Not to mention Natural Capital that continues to have the capacity to support everything that enables our socio-enviro-economic system to function!

62.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun PLACE with many economic activities PEOPLE Quality of Life PLACE is important PRODUCTS are important to satisfy needs and for quality of life ORGANIZATION for jobs is important ORGANIZATION with one operation

63.

PEOPLE need easy access to data that will improve the decisions they make …

● for themselves;

● for society; and

● for the environment.

64.

Small decisions by people make all the difference

65.

Sun Small decisions by people make all the differenceBOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun Product Place Supply Chain Process Organization Enabling environment Society

66.

FINAL WORD

There are more dimensions than just money! There are more perspectives than just the corporate organization!

67.

Almost all the data that are easily accessible for PEOPLE are those that have the corporate purpose of selling more product ... … no matter what the impact on PEOPLE, PLANET or PLACE

68.

Better metrics are essential!

69.

Sun PERSPECTIVE Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun

70.

THIS SLIDESET IS 4 OF 5

SIZE MATTERS 1 … OVERVIEW http://www.slideshare.net/PeterBurgess2/size-matters1

SIZE MATTERS 2 … KEY CONCEPTS http://www.slideshare.net/PeterBurgess2/size-matters2

SIZE MATTERS 3 … SYSTEM CYCLES http://www.slideshare.net/PeterBurgess2/size-matters3

SIZE MATTERS 4 … PERSPECTIVES

SIZE MATTERS 5 … IMPACTS http://www.slideshare.net/PeterBurgess2/size-matters5

71.

REMINDER This slideset is A WORK-IN-PROGRESS. It will be upgraded periodically. It is part of a series of more than 100 slidesets. Navigation to these is available here: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=N1-Slidesets-p3 More about the True Value Metrics initiative is at: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav FEEDBACK is welcome. Please email to Peter Burgess … peterbnyc@gmail.com … with a catchy phrase in the subject line so that it gets attention, and please identify the specific slideset(s) or webpage involved. TRUE VALUE ACCOUNTING

72. THANK YOU Some links and contact information: Email Peter Burgess … peterbnyc@gmail.com Peter Burgess LinkedIn profile https://www.linkedin.com/in/peterburgess1 Link to TrueValueMetrics.org website http://www.truevaluemetrics.org/ Link to navigation to other resources: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav#1

https://www.slideshare.net/PeterBurgess2/size-matters4

/////////////////////////////////////////////////////////////////

SIZE MATTERS-5

180 views

Share Like Download ...

Peter Burgess

Peter Burgess, Founder/CEO at TrueValueMetrics developing Multi Dimension Impact Accounting

Follow

Published on Feb 21, 2016

SIZE MATTERS 5 ... IMPACTS

A workshop at MIT to link mathematics with the

...

Published in: Data & Analytics

0 Comments

0 Likes

Statistics

Notes

no profile picture user

Share your thoughts…

Post

Be the first to comment

SIZE MATTERS-5

1.

SIZE MATTERS 5 - IMPACTS

File: TVA-p3-01-SIZE-MATTERS-2-160220.odp Peter Burgess (c) All rights reserved

2.

CONTEXT This slideset is a Work-in-Progress and will be updated from time to time. It is part of a series that aims to enable better metrics for the complex socio-enviro-economic system that we all live in. Metrics are powerful, but they must be the right metrics.

3.

IMPACTS are the result of decisions that are made by people. Change has to be driven by every human being making better decisions.

4.

The Socio-Enviro-Economic System is very complex, and in this situation, small decisions can have a big IMPACT and in ways that are difficult to anticipate accurately.

5.

The system has these components:

● Human Capital;

● Financial Capital;

● Man Built Capital*; and

● Natural Capital

and each of these is made up of many elements all of which are inter-connected in some way … * Sometimes referred to as MBSS – Man Built Structures and Systems

6.

ELEMENTS OF THE SYSTEM by SEGMENT Financial Capital Human Capital Man Built Structures & Systems Natural Capital MoneyFood Government Nature (life) Sun Nature (life) Capital Market Value Water Laws. Rules Nature (life)Land Shelter Infrastructure WaterClothes Industry Nature (life)Air Health Mining Ecoservices Education EnergySkills Waste Recreation Retail Culture LogisticsReligion Knowledge Technology Security Energy Mobility Profit TRUE VALUE ACCOUNTING SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun

7.

Human activity … man built structures and systems … change the STATE of the elements of the system along these lines …

8.

Resource extraction which depletes resources Super Rich Industrial Mining Energy Government Not-for-Profit Paperwork Banking Water Air EcoServices Habitat Law Minerals Energy Land Buildings and infrastructure do good but degrade environment Products are used to enhance Quality of Life for People Financial Losses and Profits Renewables Waste creation and its use as a resource Sun STATE Beginning of Period Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun STATE End of Period Employment contributes to Society … unemployment destroys TRUE VALUE ACCOUNTING SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun Industrial Mining Energy Government Not-for-Profit Paperwork Banking Water Air EcoServices Habitat Law Minerals Energy Land Degradation or Improvement Quality of Life Degradation or improvement of the environment BoP Affluent Super Rich BoP Affluent Impact of Activities Bad Impact Good Impact

9.

The next series of slides ... STATE BOP … ACTIVITY … STATE EOP Shows how an individual optimizes his/her performance relative to quality of life … but at the same time is having a lot of impact on everything else.

10.

ACTIVITIES OF AN INDIVIDUAL Input of Human Capital: Time, Effort, Skill, Ability, Knowledge Improves Society Improves MBSS Pro Good Activities Buy and Use PRODUCTS e.g. Food, Energy Shelter, Transport Pro Money Activities e.g. Paid Work Non-Impact Recreation Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun Improves QoL and Human Capital WASTE Liquid Gases Solids Natural Capital Depleted Maybe improves FC in HC Financial Capital Human Capital Man Built Capital Natural Capital Sun INPUTS ACTIVITIES BAD Impact State-EOPState-BOP GOOD Impact Use of MBSS Use of Natural Capital Use of Solar TRUE VALUE ACCOUNTING

11.

Job-Money Work Housing Health Time Skills Income Recreation Education ProGood Work Energy PLUS opportunities Improves society Food Clothes Resource Depletion Environmental Degradation BOP EOPThe Individual Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun PERSONAL ASSETS Energy Health Enjoyment Skills Experience Family Shelter Friends Money Stuff QUALITY OF LIFE Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun PERSONAL ASSETS Energy Health Enjoyment Skills Experience Family Shelter Friends Money Stuff QUALITY OF LIFE PRODUCTS use MBSS PRODUCTS Impact NC PRODUCTS Use MBSS PRODUCTS improve QOL TRUE VALUE ACCOUNTING

12.

Sun Small decisions by people make all the differenceBOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun MEWHAT I BUY WHERE I WORK WHERE I LIVE The supply chain for PRODUCTS HOW I USE THINGS The post use waste chain Decisions about what I buy or don't buy are of great importance!

13.

Sun Use of Pesticides Use of Land The IMPACT of FOOD Use of Water Use of Fertilizers Air Pollution Use of Growth Hormones and Antibiotics Use of Energy Use of Equipment Use of Labor Inputs Money Price Money Profit Money Cost True Value Value Add True Cost Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun Good food improves wellness Wellness improves quality of life INPUTS ACTIVITIES BAD Impact GOOD Impact

14.

Sun Use of Land The IMPACT of ENERGY Use of Water Use of Finite Resources Air Pollution Use of Energy Use of Equipment Use of Labor Inputs Money Price Money Profit Money Cost True Value Value Add True Cost Sun BOP Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Capital Natural Capital Sun Good food improves wellness Wellness improves quality of life Undue influence and corruption Land and water pollution INPUTS ACTIVITIES BAD Impact GOOD Impact

15.

Sun LAND USE Sustainable agriculture Water purification About LAND USE Wetlands Intensive monoculture Coastal mangrove Urban infrastructure Roads, Parking Lots There is a limited amount of land There are multiple possible uses Money Profit Land is a factor in improving human capital, producing goods and services, locating MBSS, and providing very critical ecosystem services Suburban sprawl Housing Tropical forest Habitat Industrial operations File: MDIA-Framework-004-150411-WIP.odp Peter Burgess (c) All rights reserved Sun BOP Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun

16.

Sun WATER USE Food production uses water Beverage production uses water About WATER USE Water is essential to LIFE Nothing is more important Household water use essential Industrial processes use water Rainfall and fresh water are abundant in some places but not everywhere Household waste also pollutes Waste water pollution from processes a critical issue Important for all processes to treat water before discharge Water is abundant, but most has too much dissolved salts to be potable Sun BOP Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun

17.

Sun EMISSIONS SO2 … acid rain CO2-Greenhouse Gas About ATMOSPHERIC POLLUTION Air pollution has many forms, all of which are more or less detrimental to people and planet Particulates MH4-Methane-GHG Some emissions have a direct impact on health Nitrous oxides Freon-ozone layer damage Some emissions are greenhouse gases that cause global warming The atmosphere is not an infinite free dump for undesirable and toxic emissions All emissions have a cost Sun BOP Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun SunSun EOP Financial Capital Human Capital Man Built Structures & Systems Natural Capital Sun

18.

MBSS Man-Built Structures & Systems Sun Natural Capital FINANCIAL ACCOUNTS Human Capital MBSS Man-Built Structures & Systems Sun Natural Capital Human Capital Economic Activity … Process Accounts REVENUES Products Sold X Price Products Bought X Price BOP EOP Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit REVENUES Products Sold X Price VALUE to buyer Equals HUMAN CAPITAL ADD Wages and benefits What value to employee? Pro-good expenditures What value to society? Taxation What value to society? For products and energy bought and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation POSITIVE IMPACT NOT ACCOUNTED FOR Negative impact

19. THIS SLIDESET IS 5 OF 5

SIZE MATTERS 1 … OVERVIEW

http://www.slideshare.net/PeterBurgess2/size-matters1

SIZE MATTERS 2 … KEY CONCEPTS

http://www.slideshare.net/PeterBurgess2/size-matters2

SIZE MATTERS 3 … SYSTEM CYCLES

http://www.slideshare.net/PeterBurgess2/size-matters3

SIZE MATTERS 4 … PERSPECTIVES

http://www.slideshare.net/PeterBurgess2/size-matters4

SIZE MATTERS 5 … IMPACTS

20.

REMINDER This slideset is A WORK-IN-PROGRESS. It will be upgraded periodically. It is part of a series of more than 100 slidesets. Navigation to these is available here: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=N1-Slidesets-p3 More about the True Value Metrics initiative is at: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav FEEDBACK is welcome. Please email to Peter Burgess … peterbnyc@gmail.com … with a catchy phrase in the subject line so that it gets attention, and please identify the specific slideset(s) or webpage involved. TRUE VALUE ACCOUNTING

21.

THANK YOU Some links and contact information: Email Peter Burgess … peterbnyc@gmail.com Peter Burgess LinkedIn profile https://www.linkedin.com/in/peterburgess1 Link to TrueValueMetrics.org website http://www.truevaluemetrics.org/ Link to navigation to other resources: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav#1 TRUE VALUE ACCOUNTING

//////////////////////////////////////////////////////////////////////////////////

THANK YOU

|

|

|

|