OVERVIEW

MANAGEMENT

PERFORMANCE

POSSIBILITIES

CAPITALS

ACTIVITIES

ACTORS

BURGESS

|

BANKING

A STRUCTURAL ANALYSIS Cantercop: The Looming Liquidity Crisis and How to Fix It

Original article: https://cantercap.wordpress.com/2022/10/18/the-looming-liquidity-crisis-and-how-to-fix-it/ Peter Burgess COMMENTARY I have a bad feeling about the strength and resilience of the modern economic system ... and this article does not help any to reduce my concern. One of the things it does is to confirm that my understanding of how the major 'money markets' actually work is woefully too simplistic. Worse, my understanding may be a whole lot better than most people, including many of those actually working in the system. One of the things that is rarely brought into the conversation is the matter of 'value add' from business and trading transactions and another is the matter of taxation that is vital to resource government programs at local, State and Federal levels. I (think I) agree with most of what is contained in the article except perhaps the observations about regulations. At some level I understand the case for less regulation because it constrains the use of available resources to perhaps mitigate some negative consequence that has come from some legitimate activities, but when such regulations are taken away there are too many bad actors that will push the system to the limits and beyond and eventually and quite quickly crash the system. Many of the regulations that were eased by Treasury Secretary Robert Rouben during the Clinton administration set the stage for the banking crisis of 2008 at the end of the Bush administration. The eased regulations were welcomed by the banks, many of which went on to abuse the lack of regulation to engage in all sorts of questionable practices to generate profit ... and for all practical purposes got away with it. I do think that a 'reckoning' is coming and I do think that it is going to be aggravated by the Fed rather than mitigated by the Fed. I am more optimistic ... or is it less pessimistic ... if the Democrats remain in control of Congress. This is because the Democrats are looking to invest and support both society and the economic system as well as the environment in ways that make sense while the Republicans seem to be stuck in a policy mindset that is decades beyond its use-by date. Maybe Prime Minister Liz Truss's spectacular policy failure in the UK can be a warning. The GOP could produce much worse for the USA if they gain a comfortable margin in the upcoming modterm election. The sliver of good news is that though there is virulent inflation in the USA, and there are financial stresses that will roil the investment community, the general population is in better financial shape than it has been in a long time and the corporate business economy is in a suprisingly stong financial condition. In particular there is a huge amount of embedded profit in the products and services being acquired by consumers, much of it because of the very high energy prices and associated embedded profit. It is interesting to note that the European Union is talking a lot now about an excess profits tax to address this embedded profit problem. Peter Burgess | ||

|

The Looming Liquidity Crisis and How to Fix It

cantercapcharlie October 18, 2022 OVERVIEW

Hamstrung by onerous regulation, the commercial banking system has been a key contributor to the liquidity crunch. But for the United States, at least, this need not be the case. If our policymakers can summon the courage to roll back the industry’s more onerous and misguided regulations, our banks could be in a position to serve as a “source of strength” to our economy and mitigate much of the pain that is headed our way. You Won’t Miss Your Liquidity ’til the Fed Runs Dry Liquidity, or, rather, the lack thereof, has been a growing problem for at least the past 20 years. Our current predicament stems from a number of sources technological, institutional and regulatory. But there are three principal causes:

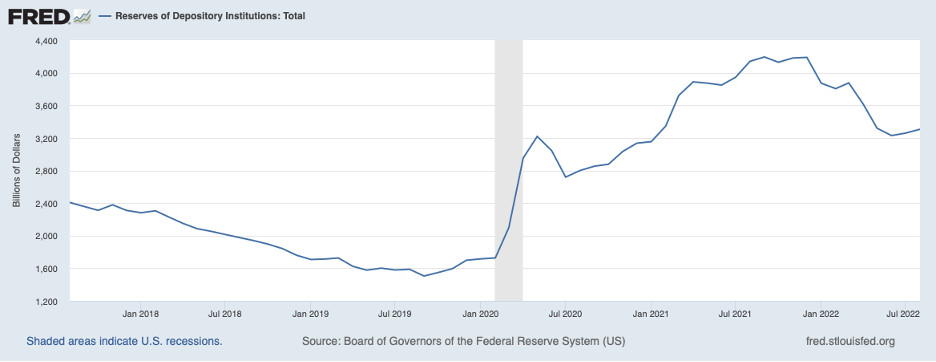

But today things are very different. Thanks to the Fed’s largesse, inflation is now a serious problem. Finally acknowledging this, the Fed recently reversed field and Is slamming on the money brakes. If the Fed responds to the next liquidity crisis by printing money, it risks losing whatever credibility it still retains. Inflation expectations could gain traction and inflation could spin out of control. “Fortress” Bank Balance Sheets Can Mitigate a Crisis Our commercial banking industry is at the heart of today’s liquidity crisis. This is ironic, because the condition of today’s banking industry is by far the strongest it has been in at least 50 years. I have been an implacable critic of bank regulation since the enactment of Dodd Frank in 2010, but no matter how much damage our hyper-regulatory regime may have done in the past decade to the banking industry and the economy, it has left us with what today is a rock solid banking system. Banks have few risky loans and far too much capital. But most importantly, banks are awash in liquidity. They just aren’t allowed to use it. Following the 2008 financial crisis, legislators and regulators imposed on the banking industry a new set of onerous regulations. Prominent among these were Dodd-Frank and the international “Basel III” capital standards. The objective of these new rules was to ensure that no bank ever again needed a “bailout.” These new regulations included strict new liquidity requirements. The idea was to immunize banks from any risk of “runs.” Banks today must contort themselves into pretzels to comply with mind numbingly obscure, arbitrary and ever-more restrictive liquidity and capital rules. An example is the “liquidity cover ratio” (LCR), which is intended to ensure that banks have sufficient cash flow to fund their maturing obligations for 30 days purely from internal funds. The end result is that banks are forced to hoard short term assets. At first glance, these strictures may seem sensible. No one wants a bank panic. There’s just one small problem; supplying liquidity is what banks do! By definition, a loan is the exchange of spending power today (a liquid checking deposit) for a promise to pay in the future (an illiquid loan contract.) Banks are the flip side of the real economy; the less liquid the banking system, the more cash is held by the public. When banks are forced to hoard liquidity, it comes out of everyone else’s pockets. Misguided Rules Force Banks to Hoard Liquidity Following are some of the ways in which banks and bank regulation are constraining liquidity: The Federal Reserve expects to remove $95 billion in bank reserves from the system every month through asset sales (more than $1 trillion in 12 months.) These reserves are considered short term assets for LCR purposes. This will force commercial banks to reduce their loan portfolios (or another longer term asset) by $95 billion. Alternatively, of course, banks could in theory borrow longer term in the capital markets. But who has the cash to lend to them?

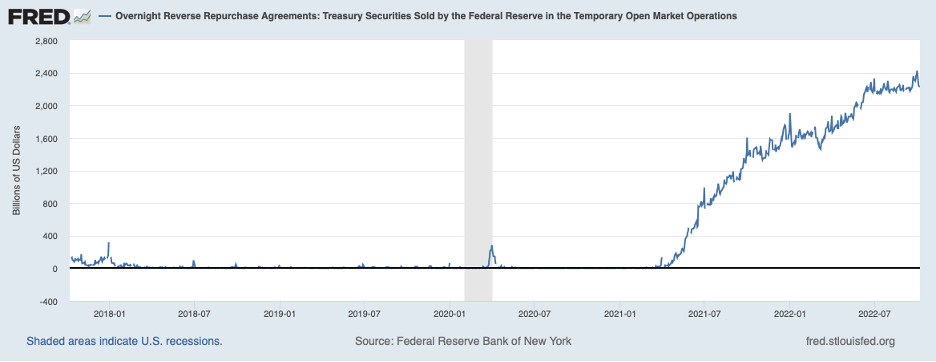

Note that even as the Federal Reserve sells securities and reduces bank reserves, it is also intentionally constraining liquidity with its $2.3 trillion reverse repo program. This program is necessary to keep overnight rates at the target level – 3.00% to 3.25%,

With short term interest rates heading toward 4%, money will flow out of retail bank deposits and into higher yielding securities and Money Market Funds. Banks can offset these retail outflows with higher-cost wholesale borrowing, but this will complicate compliance with the LCR. Banks may be obliged to reduce their lending at exactly the wrong time for the economy. A reminder: We have not yet vanquished inflation. In an inflationary environment, loan demand is likely to rise as firms buy inventory and undertake projects in advance of price increases. With their regulatory straightjackets, banks might be hard pressed to meet the legitimate borrowing needs of even their best customers, let alone new ones. “Mark-to-market” accounting standards are having a perverse impact on bank capital. As longer term interest rates rise, the value of bank securities portfolios will drop and bank equity will shrink, compelling banks to reduce lending. In the first quarter of 2022 aggregate bank equity declined by $100 billion, and certainly will have declined further in the second and third quarters. If that doesn’t sound like a big deal, consider that $100 billion is nearly ten times more than the industry lost in the entire 2008 financial crisis. To me, mark to market accounting (also known as “fair value” accounting) never made any theoretical sense. I think it violates accounting’s central “going concern” principle. But reasonable people can debate that point. More clearly pernicious is the convention that, for banks, only the asset side of the balance sheet is marked to market. If “fair value” accounting were really “fair,” liabilities would be marked to market along with assets, and bank capital would be growing, not shrinking, reflecting the actual economic value of their business. The “Volcker Rule” and related rules severely retrict the ability of banks to use their own capital to stabilize securities markets. Today, no one even pretends to be a market maker. Moreover, as noted above, since the financial crisis securities markets have grown far faster than has bank capital For nearly a decade, Quantitative Easing (QE) has artificially suppressed interest rates all along the yield curve. Its influence was especially pronounced for Treasury debt auctions, where the Fed backstopped primary dealers. Since dealers knew that the Fed “sat on the bid” to buy their inventory in the aftermarket, they could buy aggressively in auctions. They could lose a bit of money, but there was no way they could take a real bath. QT is having the opposite effect. Many bank liquidity and capital regulations are so complex and obscure and change so often that banks can never fully be certain whether they are in compliance with any regulatory threshold. In volatile times like now, prudent banks will maintain a large cushion of liquidity to avoid running afoul of impenetrable regulatory guidelines. A related issue is the heightened difficulty of managing payments, especially “daylight overdrafts.” To stay in compliance with liquidity rules, banks today must be scrupulous about avoiding unexpected end-of-the-day deficits. Again, a prudent bank will opt to maintain a redundant liquidity cushion. Banks Have Room For $5 Trillion in New Credit The banking sector’s strength means that it is well positioned to mitigate, if not prevent, any future recession. As firms struggle with the double whammy of a weakening economy and higher interest rates, many will inevitably go bankrupt or otherwise need restructuring. These days, banks have little exposure to the highest risk loan categories. Most of these sketchy credits are held by non-bank lenders (hedge funds, mutual funds, pension funds, etc.) For instance, banks have fewer construction loans than they did in 2008 both in absolute and relative terms. “Construction & Development” loans today measure 3% of loans versus 10% back then. (This largely explains our current housing shortage, but that’s a subject for another day.) Big picture, the banking industry today has $11 trillion in loans and roughly $1.9 trillion in tangible equity: equity measures 17% of loans. From 1990 to 2009, 12% equity-to-loans was the norm and proved more than adequate to endure the financial crisis. If we returned to those levels, banks would have the capacity to book an additional $5 trillion in loans without commensurate growth in their balance sheets. Bank liquidity is similarly plentiful. For as long as anyone can remember, the rule of thumb for bank liquidity has been the loan-to deposit ratio. Historically, 85-90% has been regarded as the threshold between adequate and insufficient liquidity. Today, this measure stands at 57%. Again, banks have sufficient excess deposits to fund an additional $5 trillion in new credits. With little exposure to the riskier credit categories, banks are perfectly positioned to manage debt restructurings for troubled firms. They have the balance sheet capacity, the credit expertise, and the distribution capability. Plus, managements will not be as distracted as in the past by loan workouts. But Only if Regulations are Relaxed To transform our commercial banking industry into a “source of strength” for our economy, our policymakers must resolve to roll back the most restrictive bank regulations. Beyond setting banks free to lend, there are at least three advantages to relaxing bank regulation. First, if banks are refinancing and restructuring existing credits, no new money is created. Thus, this is non-inflationary. Second, the expense and the risk of these restructurings would be incurred by the banks and their shareholders, not taxpayers. Finally, fraud will less pervasive than it tends to be with government program such as that which funded COVID relief. It’s easy for me to advise that we should “roll back existing bank regulations” but in practice this will not be so easy. It will require bending, if not breaking with, international agreements like Basel III as well as a decade of domestic regulatory accretion. Any effort to “roll back” regulations is likely to be met with fierce resistance from several constituencies intent on preserving the status quo.. Getting So Much Resistance From Behind Most importantly, the immense regulatory bureaucracy (the Federal Reserve, the FDIC, the OCC, the BIS, the ECB, the Bank of England, etc., etc.) will be loath to relinquish any of its power, let alone concede that their policies have been misguided from the get-go. Regulators have no incentive to apply any but the strictest regulations; they will not benefit if looser regulation enhances economic growth, but they certainly will lose if a large banks fails. In fact, following the June 2022 “stress tests”, regulators amplified our liquidity squeeze by hiking capital requirements for Citigroup and JP Morgan Chase. Other banks may yet receive similar treatment. Given Citi’s spotty history, I cannot quibble with that decision. But I seriously doubt that Morgan’s financial condition markedly deteriorated in the past 12 months. Every year the arbitrary stress test scenarios grow increasingly unrealistic and severe, which gives regulators a pretext to keep raising capital standards. It almost seems that their ultimate goal is to put the kibosh on bank lending altogether. Then, no bank could ever fail. The regulatory dream. In addition to the regulators themselves, an industry has evolved of attorneys, consultants, lobbyists, and academics whose livelihoods hinge on ever more arcane and oppressive regulation. Of even more concern is an assortment of legislators who have built careers around the vilification of bankers and little else. Some people will object to any relaxation of bank regulations on the grounds that deregulation caused the 2007-8 financial crisis. But this is a myth. The crisis was not caused by free markets run amok, but by bad regulation — mainly, the Basel capital standards These regulations allowed International banks, mainly European banks, to become egregiously over leveraged and illiquid. US shadow banks followed suit. Another myth about the financial crisis is that the US banking system needed a “bailout.” This myth is so deeply embedded in our national psyche as to be an article of faith for many. In fact, because US regulators back then had the wisdom to require more stringent capital reserves than did Basel, US commercial banks weathered the crisis impressively well. The maximum loss suffered by the industry was $12 billion in 2008 ($67 billion for bank holding companies.) The point is that the 2006 bank regulatory regime, however imperfect, was more than adequate: further regulation such as Dodd-Frank was simply not needed. My present working hypothesis is that Fed Chairman Powell will pursue his tightening policy until inflation breaks, letting the economic chips fall where they may. This appears to be Powell’s not-so-hidden agenda; his rhetorical emphasis on “Pain” would not seem to presage a soft landing. Recession seems baked in the cake. One caveat: Powell’s priorities may change if a liquidity crisis first hits foreign, and especially emerging debt markets. Right now, this seems highly likely. Soaring US interest rates have driven the dollar to record highs, so emerging economies will be hard pressed to service or refinance their dollar- based debt. Chair Powell might well feel compelled to supply dollars to avert sovereign defaults, thereby abandoning his inflation-fighting strategy. This could defer a recession temporarily, but might ultimately bring something worse: stagflation or an even deeper recession. To conclude; thanks to over-regulation, sound management, and sheer serendipity, the United States is extraordinarily fortunate to have a commercial banking industry capable of serving as a source of strength in a recession. But to capitalize on this good fortune, we must immediately roll back the industry’s more draconian regulatory constraints and return business decisions to bank managers. There is no substantive reason not to do so. It could easily mean the difference between a soft landing and economic carnage. ---------------------------------- Who I Am I've been a bank geek for nearly 40 years. 'Sell-side' experience at Keefe Bruyette, Goldman Sachs, and Lehman Bros. (RIP). Investor at 4 funds, two of which I founded. Lending experience at First National State Bank of Newark, NJ. Why the fascination with banking? A sickness, I suppose. More likely, it was my dad, an economist who wrote his doctoral dissertation on canal construction and finance in the 1820's and 1830's. To understand the financial crisis and today's financial world, one could do worse than study the panic of 1837. I'll share one of my dad's admonitions which still rings true: 'Charlie, economists have solved every important economic problem except two; they don't know where growth comes from and they don't know where inflation comes from.'

| The text being discussed is available at | https://cantercap.wordpress.com/2022/10/18/the-looming-liquidity-crisis-and-how-to-fix-it/ and |