Date: 2024-12-21 Page is: DBtxt003.php txt00019883

Economics

John Mauldin

Thoughts from the Frontline - The Great Reset vs. The Great Reset

Peter Burgess

John Mauldin

John Mauldin A quick note before I start: Some of you didn’t get last week’s letter because some major internet providers decided it was junk mail. This was maddening but beyond our control. It may be in your “spam” or junk folder. You can help us train the algorithms by marking them as “not spam.”

Remember, you can always read my letters on our website, www.MauldinEconomics.com, anytime, along with all my prior letters. And there’s some good stuff there from the rest of our team. Now, on to the letter.

In baseball, there is a situation where a base runner is sprinting to home plate and can’t see what is happening behind him. Totally focused on scoring, he doesn’t know if the outfielder is throwing a ball that will reach home plate first. That’s where we get the phrase “out of left field.” (If the ball were coming from right field, the runner could actually see it.)

COVID-19 was the ultimate ball out of left field. Yes, we knew viruses spread and pandemics were possible. Most of us have lived through them before. We didn’t foresee this particular one appearing when and where it did. But it quickly changed the course of history.

Or did it? In the grand scheme of things, maybe not. World-changing trends were already in motion and are continuing. The pandemic may delay or more likely hasten events, but not stop them. For instance, I think The Great Reset is still coming. I previously expected we would get through to at least the late 2020s before hitting the debt wall. Now, I’m not so sure. This pandemic and recession may push us there faster because they are making the debt grow faster.

Today I’m going to blend a few thoughts about The Great Reset with some other historical analysis I recently discovered. It adds up to a disturbing outlook, even if (as seems likely, given the latest vaccine news) we’re past the pandemic by late next year. We’ll find different challenges on the other side.

“Revamp” Capitalism

Whenever I mention The Great Reset (most recently here), people ask me to explain exactly what it will look like. I can’t answer because I don’t know in terms that can be labeled “exact.” The Great Reset is simply my term for climactic events that resolve our global debt overload while at the same time dealing with slow economic growth, high unemployment, and social unrest. It could happen many different ways, some better than others. But I firmly believe we will see some kind of resolution. The present course is unsustainable.

Another source of confusion is that I’m not the only one to use this term. Others have used it for their own purposes.

You probably know of the World Economic Forum, whose annual soiree in Davos, Switzerland gathers the world’s wealthy and powerful to discuss/solve our common problems. That’s what they say, at least. Somehow the problems they discuss never seem to get solved, so it’s fair to wonder what they do there. It is, however, a great way to meet fellow elites. (Somehow, my invitation keeps getting lost in the mail.)

Now, in the spirit of “never let a good crisis go to waste,” the WEF sees the coronavirus pandemic as an opportunity to reset capitalism. Really. Founder Klaus Schwab says it quite openly.

COVID-19 lockdowns may be gradually easing, but anxiety about the world’s social and economic prospects is only intensifying. There is good reason to worry: a sharp economic downturn has already begun, and we could be facing the worst depression since the 1930s. But, while this outcome is likely, it is not unavoidable.

To achieve a better outcome, the world must act jointly and swiftly to revamp all aspects of our societies and economies, from education to social contracts and working conditions. Every country, from the United States to China, must participate, and every industry, from oil and gas to tech, must be transformed. In short, we need a “Great Reset” of capitalism.

WEF calls this effort its “Great Reset Initiative.” For the record, it has nothing to do with my conception of The Great Reset. In fact, I think much of what they propose will make the version that I see even worse. I agree capitalism has gone off track and needs some adjustments, and not just minor ones. The current morass of crony capitalism and lobbying for special government favors is abhorrent. But “revamp all aspects of our societies and economies” sounds ominous. Especially coming from the people already nominally running the global economy.

Furthermore, what they really propose is that we change our lives while Davos Man continues undisturbed, maybe paying a few more taxes but with the brunt of the change affecting those further down the food chain. And, of course, they are not long on specifics.

When you start talking about resetting the educational and social contracts and working conditions, you are talking a radical social agenda. I believe we are going to have to have considerable change in the social structure of this country. That is what the current partisan politics is telling us. Too many people on both sides feel the current “social contract,” whatever you might think it is, is not working for them. Income and wealth inequality are very real. I am not convinced a WEF-style “Great Reset” is the answer.

Fortunately, I don’t think WEF will get very far. More likely, this is another example of wealthy, powerful elites salving their consciences with faux efforts to help the masses, and in the process make themselves even wealthier and more powerful.

The real problem may be simpler: We have too many “elites.” History shows this rarely ends well.

Excess Elites

The December issue of The Atlantic magazine has a fascinating interview with Peter Turchin, a University of Connecticut professor with some unique ideas about human history.

Turchin is actually a zoologist. He spent his early career analyzing population dynamics. Why does a particular species of beetle inhabit a certain forest, or why does it disappear from that same forest? He developed some general principles for such things, and wondered if they apply to humans, too. Answering that requires data, so he went from studying beetle history to human history.

One recurring pattern, Turchin noticed, is something he calls “elite overproduction.” This happens when a society’s ruling class grows faster than the number of rulers it needs. (For Turchin, “elite” seems to mean not just political leaders but all those managing companies, universities, and other large social institutions as well as those at the top of the economic food chain.) As The Atlantic describes it:

One way for a ruling class to grow is biologically—think of Saudi Arabia, where princes and princesses are born faster than royal roles can be created for them. In the United States, elites overproduce themselves through economic and educational upward mobility: More and more people get rich, and more and more get educated. Neither of these sounds bad on its own. Don’t we want everyone to be rich and educated? The problems begin when money and Harvard degrees become like royal titles in Saudi Arabia. If lots of people have them, but only some have real power, the ones who don’t have power eventually turn on the ones who do…

Elite jobs do not multiply as fast as elites do. There are still only 100 Senate seats, but more people than ever have enough money or degrees to think they should be running the country.

“You have a situation now where there are many more elites fighting for the same position, and some portion of them will convert to counter-elites,” Turchin said.

The excess elites become counter-elites, who then try to make alliances with the lower classes which usually don’t work out. But my eyebrows went up when I saw how Turchin describes the endgame.

The final trigger of impending collapse, Turchin says, tends to be state insolvency. At some point rising insecurity becomes expensive. The elites have to pacify unhappy citizens with handouts and freebies—and when these run out, they have to police dissent and oppress people. Eventually the state exhausts all short-term solutions, and what was heretofore a coherent civilization disintegrates.

Terrifying? Yes. It sounds amazingly like what the WEF proposes. I am sure Klaus Schwab and the others there recognize the frustration that many people have. They are proposing programs to alleviate that frustration—expensive, society-altering programs. But they would still let the game at the top continue.

But it gets worse.

Instability Spikes In 2010, the scientific journal Nature published a collection of opinions looking ahead 10 years, i.e., where we are right now. Nature then published a short response from Turchin in its February 2010 issue.

Quantitative historical analysis reveals that complex human societies are affected by recurrent—and predictable—waves of political instability (P. Turchin and S.A. Nefedov, Secular Cycles, Princeton Univ. Press; 2009). In the United States, we have stagnating or declining real wages, a growing gap between rich and poor, overproduction of young graduates with advanced degrees, and exploding public debt. These seemingly disparate social indicators are actually related to each other dynamically. They all experienced turning points during the 1970s. Historically, such developments have served as leading indicators of looming political instability.

Very long 'secular cycles' interact with shorter-term processes. In the United States, 50-year instability spikes occurred around 1870, 1920, and 1970, so another could be due around 2020. We are also entering a dip in the so-called Kondratiev wave, which traces 40-60-year economic growth cycles. This could mean that future recessions will be severe. In addition, the next decade will see a rapid growth in the number of people in their twenties, like the youth bulge that accompanied the turbulence of the 1960s and 1970s. All these cycles look set to peak in the years around 2020.

Again, that was from 2010. Right on schedule, we are experiencing the “instability spike” Turchin says tends to come along every 50 years.

Why 50 years? It relates to the human lifespan. Consider who was “in charge” during the period around 1970. We Baby Boomers were all 25 or younger at the time. Managing the chaos fell on older generations, who remembered it well and spent the rest of their lives trying to prevent more of it. But after 50 years or so, they are mostly gone. We who remain must learn the lesson again.

I’ve talked before about Neil Howe’s “Fourth Turning” idea, and George Friedman’s geopolitical cycles, both of which are peaking in this decade. Interestingly, Friedman also sees a different geopolitical 50-year cycle playing out in the mid- to late ‘20s. Which overlaps with his 80-year geopolitical cycle for the first time. The mid- to late ‘20s should see the climax of Neil Howe’s Fourth Turning. Now we see Peter Turchin postulating a similar time frame for different reasons. None of them, to my knowledge, expected the pandemic we are now experiencing. What is its effect?

Well, we know the pandemic triggered a recession that may, before it’s over, rival the Great Depression. For millions of Americans, it is not just something they read about. They feel it.

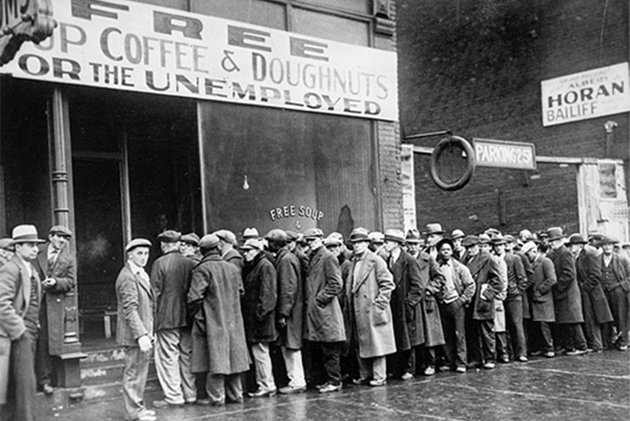

You’ve probably seen this famous 1931 photo of Al Capone’s Chicago soup kitchen.

Source: Wikimedia

The 2020 equivalent is this from my former hometown Dallas last week. That was very emotional for me and brought a tear to my eye.

Source: CBSDFW via Twitter

We do see progress in these images. The people obviously have cars and fuel. Those were elite luxuries in 1931. Some of these people may be educated and intelligent, but they’re not elites. Actual elites don’t have to wait in line for food. They call Whole Foods or DoorDash and have it delivered.

The problem, borrowing Turchin’s framework, is that some thought they were elites, or if not exactly thinking of themselves as elite, did enjoy the benefits of good jobs, at least until recently. This year took away that illusion, and they’re naturally disappointed. They may join the “counter-elites” and seek more power.

This is where we are. The hard times we’ve long anticipated are here. That 1931 soup kitchen photo was just the beginning of a long, dark period. It got a lot worse.

Will our situation similarly worsen? That remains to be seen. As I’ve said, good things keep happening even in the darkness. The mRNA technology behind the new coronavirus vaccines may lead to breakthrough treatments for other conditions. mRNA technology allows the delivery of specific proteins to the human body. If you have a disease, and there are many of them that simply come along as part of the process of aging, it may soon be possible to deliver specific proteins that cure or at least mitigate your condition.

I want to further explore Peter Turchin’s ideas, but in fairness to him, I want to read more of his work first. He has a number of books and articles. I will even try to reach out for discussion. What I see so far is worth deeper study.

But the more important part is that I especially pay attention when I see multiple smart people reaching similar conclusions for different reasons. We are now at what Turchin calls the final stage, when elites try to pacify the masses with bread and circuses. Doing so racks up the debt and suppresses economic growth. Debt is accumulating faster than I expected, so The Great Reset may happen sooner than I expected.

Whenever it comes, we should welcome it. The alternatives may be even worse.

What Do We Do with All That Debt?

But that still doesn’t answer the question that is on our minds: What happens when we come to the place where we have to deal with all that debt? Fortunately, my favorite central banker, Canadian Bill White who was the BIS chief economist, did a brilliant interview with my friend Mark Dittli in Switzerland this week which gives us some answers.

Today, the Canadian criticizes the central banks: “They have pursued the wrong policies over the past three decades, which have caused ever-higher debt and ever greater instability in the financial system.” He suggests that the current crisis should be used to rethink in order to build a more stable economic system, one in which fiscal policy plays a greater role and that relies more on productive investment. In this in-depth conversation, White says what should be done—and he demands more humility from decision-makers: “We know much less about the economy than we think we do.”

But Bill is not calling for austerity at this time. He recognizes we are in a recession/potential depression. But he wants more emphasis on the fiscal policy and not central banks.

We’re on a slope where monetary policy has become increasingly ineffective in promoting real economic growth. Every crisis was met with monetary easing that caused debt and other imbalances to accumulate over time, and that caused the next crisis to be bigger than the previous one. The next crisis then needed more punch from central banks. But since interest rates were never raised as much in upturns as they were lowered in downturns, the capacity to deliver that punch was decreasing.

[The recent March, 2020] episode perfectly encapsulates my view of what’s wrong with our monetary policy of the past decades. True, the Fed had no choice but to step in to prevent a financial meltdown. But this meltdown only happened because of the monetary policy followed over previous years.

… my point is: Central banks create the instabilities, then they have to save the system during the crisis, and by that they create even more instabilities. They keep shooting themselves in the foot.

William Dudley and other central bankers are beginning to admit that they have come to the end of their effective ability to manage their respective economies. Governments have to step in with fiscal policy that is actually targeted and productive.

Then Bill lists four ways that we can deal with the debt, not all of them palatable:

There is no return back to any form of normalcy without dealing with the debt overhang. This is the elephant in the room. If we agree that the policy of the past thirty years has created an ever-growing mountain of debt and ever-rising instabilities in the system, then we need to deal with that.

In theory, there are four ways to get rid of an overhang of bad debt. One: Households, corporations and governments try to save more to repay their debt. But we know that this gets you into the Keynesian Paradox of Thrift, where the economy collapses. So this way leads to disaster. Two: You can try to grow your way out of a debt overhang, through stronger real economic growth. But we know that a debt overhang impedes real economic growth. Of course, we should try to increase potential growth through structural reforms, but this is unlikely to be the silver bullet that saves us. This leaves the two remaining ways: Higher nominal growth—i.e., higher inflation—or try to get rid of the bad debt by restructuring and writing it off.

When later asked about write-offs he said this:

That’s the one I would strongly advise. Approach the problem, try to identify the bad debts, and restructure them in as orderly a fashion that you can. But we know how extremely difficult it is to get creditors and debtors together to sort this out cooperatively. Our current procedures are completely inadequate.

I expect that we will be coming back to this interview again. (Over My Shoulder members can read my marked copy here.)

How long can this go on? Longer than you might think. From Rosie (David Rosenberg) Friday morning:

We had core CPI data out of Japan and the YoY trend went further into deflation to -0.7% in October from -0.3% in September. The is the sharpest move into deflation terrain since March 2011. A country with a 700% total debt-to-GDP ratio, two decades of zero interest rates, and a central bank balance sheet that is 130% of GDP. Nice to see how all the credit creation has managed to spur on a reflationary backdrop. Shades of what’s to come in the US.

I agree. The US could turn Japanese. While I think we could see inflation in the short term (2 to 3 years) the debt overhang and growth of central bank reserves will lead us directly into the same problem Japan is facing: a deflationary economic cycle with no growth. All while new technology (especially biotechnology) makes our lives better. It will be a strange new world that will have no resemblance to the last decade’s “normal.”

We will stumble through and some of us will do extraordinarily well, because we position ourselves to take advantage of this cycle. Stay tuned…

Thanksgiving Gift

To get through this time you need good, solid investment information. We have quite a bit of it at Mauldin Economics, but we know budgets are tight. We’re going to help by holding an online “Open House” next weekend for some of our most popular premium services. For just a brief time, you’ll get to peek at top analysis and specific recommendations, with no obligation at all.

Watch for an email from us next Thursday morning. It will tell you how to claim this Thanksgiving gift… and that’s truly what it is. I am thankful for you and I hope this information helps you through the coming turbulent years.

Holiday in Puerto Rico

Up until last weekend, I was planning to fly to Dallas for Thanksgiving with my kids. But in a discussion with my doctor, Mike Roizen, he looked at an app on his phone that analyzed the conditions I would face on the trip. It showed something like a 60% chance I would encounter someone who was asymptomatic but possibly contagious. That just didn’t seem like good odds to me. And while Thanksgiving is my favorite holiday, I would like to spend another 40 to 50 (minimum) years celebrating Thanksgiving with my kids and grandkids and great grandkids. So this year, Shane and I will visit with our kids over Zoom and maybe meet (safely) with a few neighbors.

However you spend Thanksgiving, have a great week and stay safe. I take comfort in the fact that the vaccine news seems more encouraging every day. This time next year, at least parts of our world should be back to normal.

Your still positive about the future of humanity but not so much government analyst,

John Mauldin

John Mauldin John Mauldin

Co-Founder, Mauldin Economics

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.